Life is unpredictable. Your car breaks down. Your roof starts to leak. You lose your job. These unexpected events can quickly derail your financial situation — unless you have an emergency fund.

What is an Emergency Fund?

An emergency fund is money set aside to cover unexpected expenses or financial emergencies without going into debt. Financial experts typically recommend saving 3–6 months of living expenses.

Why You Need an Emergency Fund

An emergency fund helps you in many ways:

- Prevents debt cycles: You can handle unexpected costs without resorting to high-interest credit cards or loans.

- Reduces stress: Knowing you have a financial safety net for emergencies gives you peace of mind.

- Protects other financial goals: You won't need to dip into retirement savings or investment accounts when emergencies happen.

- Creates financial stability: It makes you more resilient in the face of job loss, medical bills, or major repairs.

How Much Should You Save?

The standard recommendation is 3–6 months of essential expenses. Start with a starter emergency fund of $1,000, then build toward the full amount. For most people, essential monthly expenses include: housing, utilities, groceries, transportation, minimum debt payments, and insurance.

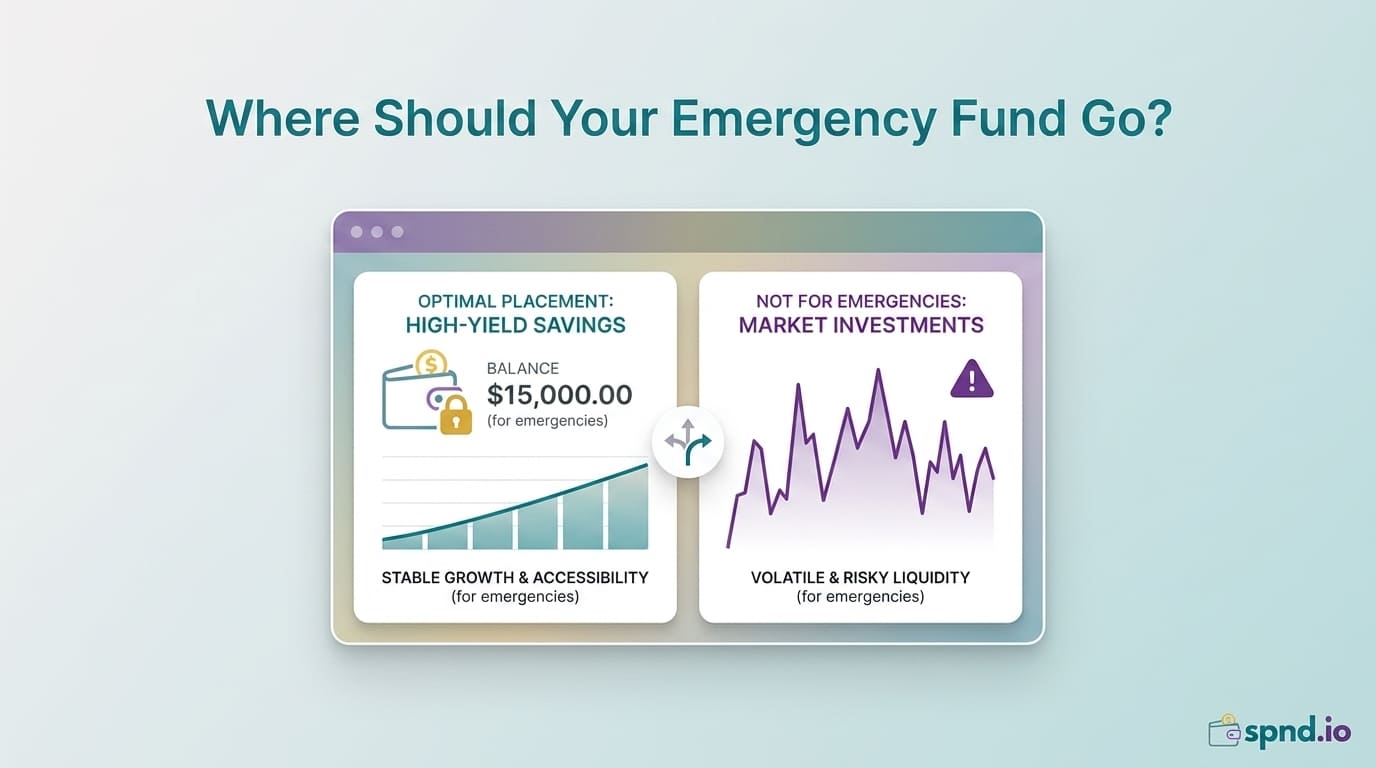

Where Should You Keep Your Emergency Fund?

Your emergency fund should be: liquid (easily accessible when needed), safe (not subject to market fluctuations), and separate from your regular checking account to avoid temptation. A high-yield savings account with a no-fee bank is a great option. You can find no-fee options in our No-Fee Bank Directory.

Step-by-Step Guide to Building Your Emergency Fund

1. Set a clear target

Calculate your monthly essential expenses and multiply by 3. That's your initial target. Start with $1,000 if full funding seems overwhelming — just get started.

2. Make room in your budget

Use our Budget Planner to identify expenses you can reduce or eliminate temporarily. Cutting one restaurant meal a week or cancelling an unused subscription could add $50–$100 to your emergency fund monthly.

3. Automate your savings

Set up automatic transfers to your emergency fund right after payday. Even $25 a week adds up — you'll have over $1,300 in a year. For the fastest results, deposit your emergency fund contributions immediately after you receive your paycheck.

4. Boost your fund with windfalls

Contribute at least 50% of unexpected income to your emergency fund, such as: tax refunds, work bonuses, cash gifts, and side hustle income.

5. Track your progress

Use our Cashflow Planning Tool to monitor your emergency fund growth. Celebrating small milestones like hitting $500 keeps you motivated.

6. Only use it for true emergencies

Be disciplined about what counts as an emergency. True emergencies include: job loss, medical emergencies, essential car repairs, major home repairs like a broken furnace, and critical appliance replacement.

The Bottom Line

An emergency fund is the cornerstone of financial stability. It's the foundation that every other financial goal is built upon. Start small, be consistent, and remember: something is always better than nothing. Even a $500 emergency fund can prevent you from going into debt over a car repair or medical bill.

Begin building yours today — your future financially secure self will thank you.