The most reliable way to get rich slowly has nothing to do with investing skill, market timing, or discipline. It is automation — the unglamorous practice of building a financial system that makes good decisions for you on autopilot so you do not have to make them fresh every paycheck.

This post walks through exactly what to automate, in what order, and how to set it up in one afternoon so that the decisions you want to make consistently for the next 30 years happen without you thinking about them.

Why Manual Fails and Automatic Wins

If you rely on willpower, here is a typical month: paycheck lands. You intend to transfer $400 to savings. Something comes up — a birthday, a slow Tuesday, an unexpected expense. You'll do it next week. Next week becomes next month. Six months later you have saved $200 instead of $2,400.

Automation removes the 'decide every time' problem. You decide once, set up the transfer, and the decision makes itself every payday for the rest of your life until you change it.

A large Vanguard study tracking 401(k) participants found that automatic enrollment and automatic contribution increases roughly triple long-term retirement account balances compared to opt-in systems. The participants' willingness to save was similar — only the default and the automation were different. That single structural change turned decent savers into great ones.

The Automation Stack

A complete automation stack has four layers, each one protecting you from a different failure mode.

Layer 1: Income splitting on payday

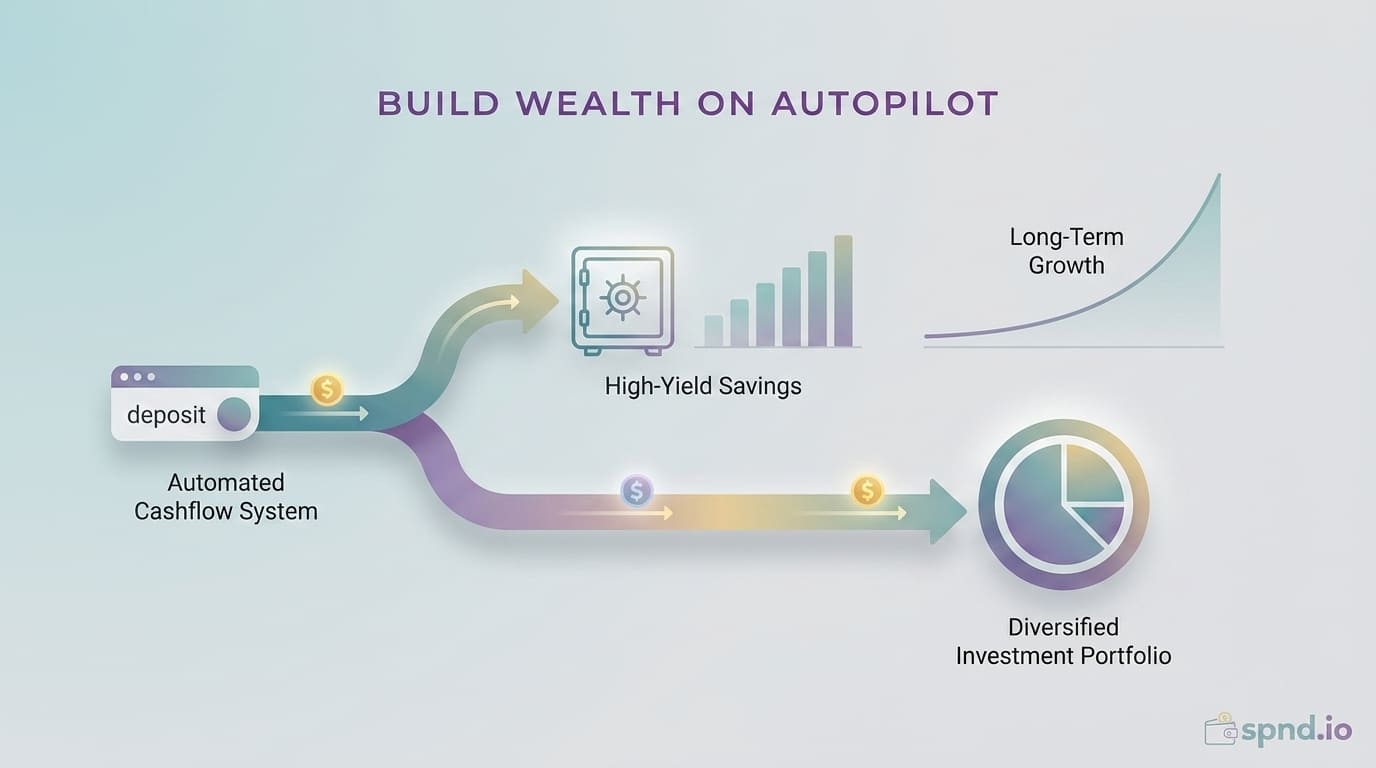

The moment your paycheck hits, a predetermined amount moves out to designated accounts — before you can see it, before you can 'decide' to spend it. This is the foundation. Everything else builds on it.

Layer 2: Bill auto-pay

Every recurring bill — rent or mortgage, utilities, insurance, subscriptions, credit card minimums — pays itself automatically. No late fees, no missed payments, no mental bandwidth consumed.

Layer 3: Investment auto-purchases

Money that hits your investment account does not sit in cash — it automatically buys whatever fund or portfolio you have selected. Most brokerages support scheduled investment purchases now.

Layer 4: Automatic increases

The most underused layer. Your automated savings amount increases by 1% or 2% every year without you doing anything. Over 10 years, this alone can double your savings rate without ever feeling a specific reduction in lifestyle.

The Priority Order (Everything in One Place)

When you set up automation, direct the money to the right places in the right order:

-

Employer 401(k)/RRSP match (free money — automate to the full match, always)

-

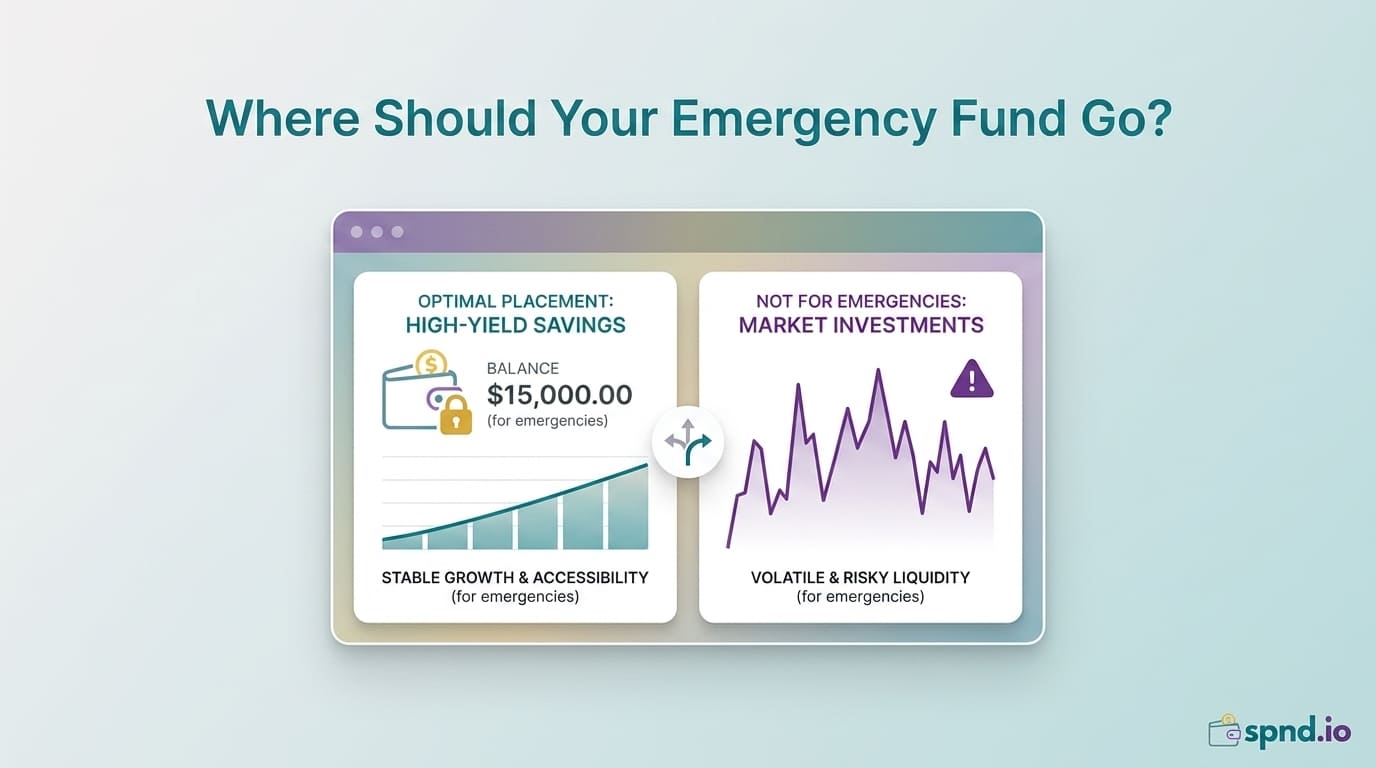

Starter emergency fund ($1,000-$2,000) in a high-yield savings account

-

High-interest debt payoff (credit cards above 15%)

-

Full emergency fund (3-6 months of essential expenses)

-

Max out tax-advantaged retirement accounts (Roth IRA in US, TFSA in Canada)

-

Max out 401(k) or RRSP beyond the employer match

-

Taxable brokerage account for additional long-term investing

-

Other goals: down payment fund, education savings, etc.

This order is not rigid — adjust for specifics. The principle: automate the highest-priority unfilled goal first. Once it is filled, redirect that automated flow to the next goal. The total 'savings rate' stays constant, but where it lands evolves over time.

The Specific Setup: One Afternoon

In most cases, the full stack can be set up in 3-4 hours of focused work across two sessions (morning to gather accounts and info, afternoon to configure). Rough plan:

Session 1 — Gather (45-60 minutes)

-

List every account you have: checking, savings, retirement, investments, loans, credit cards

-

Write down your take-home pay and pay frequency

-

Calculate your automation budget: emergency fund contribution, retirement contribution, savings goals. Use the 50/30/20 rule if you have no baseline.

-

Identify any accounts you still need to open (high-yield savings, IRA/TFSA, brokerage)

Session 2 — Configure (2-3 hours)

-

Open any missing accounts (high-yield savings, retirement account, brokerage)

-

Set up direct deposit splits if your employer supports them — can send portions of paycheck directly to different accounts

-

If splits not available, set up recurring transfers from checking to each destination, timed 1-2 days after payday

-

In each investment account, set up automatic purchases of your chosen fund (target-date fund or broad index fund)

-

Enable auto-pay on every bill and credit card minimum

-

Set a calendar reminder for 12 months out: 'Increase automated savings by 1%'

The 'One Afternoon' That Builds Decades

The math of this single afternoon is almost absurd.

Consider a 30-year-old earning $5,500/month net, automating 20% of income ($1,100/month) into retirement and investment accounts at a 7% annual return.

-

After 10 years: ~$190,000

-

After 20 years: ~$570,000

-

After 30 years: ~$1,340,000

-

After 35 years (age 65): ~$1,900,000

The time cost of setting this up was one afternoon. The ongoing time cost is zero — you review once a year for a few minutes. The outcome is a seven-figure retirement account that a different version of you, who meant to save but never quite got around to it, would not have.

What Automation Actually Frees Up

The surprising benefit is not financial — it is mental. People who have automated their financial lives consistently report:

-

Less money anxiety in general (the system is working, you do not need to think about it daily)

-

Less decision fatigue (fewer small money decisions per week)

-

Less marital friction for couples (transparent, shared system removes the 'who forgot to pay' arguments)

-

More confidence to make bigger financial moves (career changes, sabbaticals, entrepreneurship) because the foundation is stable

Common Automation Mistakes

Mistake 1: Automating too much too soon

Automating 30% of income in the first month usually fails when a real expense hits. Start at 10-15%, live with it for 2-3 months, then step up. Automation only works if it is sustainable.

Mistake 2: Forgetting to increase contributions

Most people set up automation at one amount and never touch it again. Raises, life changes, and reduced expenses should trigger increases. Easy fix: annual calendar reminder.

Mistake 3: Not reviewing quarterly

Automation is not 'set and forget forever.' Set and review quarterly (15 minutes per quarter): check that transfers are running, check account balances, adjust if life changed significantly.

Mistake 4: Automating savings but not automating investing

Money that automates to savings but sits in cash earns 4% at best. Money that automates to a retirement account but stays in cash earns the same. The automation has to go all the way through — money hits the account, auto-buys the fund. Check this setting; it is frequently missed.

Mistake 5: Not naming accounts clearly

'Savings Account 1' does not tell you what it is for 2 years later. Rename accounts by purpose: 'Emergency Fund,' 'House Down Payment 2029,' 'Wedding Fund.' When purposes are clear, you do not accidentally raid the wrong account.

Automation for Variable Income

Freelancers and commission workers often think automation does not work for them. It works — it just needs a different structure.

Use a business account as the 'paycheck' source. Pay yourself a fixed monthly salary from the business account to a personal checking account, timed on a consistent day. From the personal account, automate the same way a salaried person does. The business account absorbs the variability; personal automation stays steady.

The Real Takeaway

Nobody builds wealth by being amazing at money every single day for 30 years. They build wealth by being pretty good at money on one specific afternoon, setting up a system that makes good decisions for them by default, and then mostly leaving it alone for decades.

If you take one thing from this article: book a 3-hour block this weekend. Set up the automation stack. It will feel like a minor administrative task while you are doing it. Thirty years from now it will be the single most important financial move you made in your entire life.

Start the one-afternoon setup today. Use the spnd.io Budget Planner to set your automation amounts, the Retirement Calculator to see your 30-year trajectory, and the No-Fee Bank Directory to open the right accounts at the right banks. Decide once, benefit for decades.