If you have ever tried to budget and given up within two weeks, you are in good company. Most budgeting systems fail for the same reason: they treat every dollar like a tiny accounting problem. The 50/30/20 rule skips the line-by-line pain and replaces it with three buckets you can actually remember.

This guide walks through exactly what the 50/30/20 rule is, how to apply it to your real paycheck, where people get it wrong, and when it does not work. By the end you will have a working split for your income, a plan for the savings portion, and a way to check your progress every month without a spreadsheet that makes you want to quit.

What is the 50/30/20 Budget Rule?

The 50/30/20 rule is a budgeting framework that splits your after-tax income into three fixed percentages. Fifty percent goes to needs, thirty percent goes to wants, and twenty percent goes to savings and debt repayment beyond the minimums. That is the whole system.

It was popularized in the 2005 book All Your Worth by Elizabeth Warren and her daughter Amelia Warren Tyagi. They argued that most people fail at budgeting because traditional envelope and line-item methods require obsessive tracking. Three categories, they reasoned, is something a human can actually hold in their head.

Two decades later it is still the most widely recommended starter budget in personal finance because it hits the sweet spot between structure and simplicity. It does not tell you exactly what brand of coffee to buy. It tells you how much of your money should be going toward staying alive, enjoying your life, and building a future.

The Three Categories Explained

50% — Needs

Needs are expenses you cannot avoid without real consequences. Miss them and something breaks: you lose your home, your car gets repossessed, the lights go out, you cannot get to work.

This category includes rent or mortgage payments, utilities (electricity, water, heat, basic internet), groceries, transportation to work (car payment, fuel, insurance, transit pass), minimum debt payments on credit cards and loans, health insurance and essential prescriptions, childcare if it enables you to work, and basic clothing.

Needs does not mean 'things that feel important.' Cable TV is not a need. A gym membership is not a need (even if you use it). Organic produce at a premium price is a preference, not a need. When in doubt, ask: if I stopped paying this, would something serious happen within 30 days? If no, it belongs in the next bucket.

30% — Wants

Wants are everything that makes life actually worth living but that you could, in a pinch, cut. Dining out, streaming services, concert tickets, vacations, the better phone plan, hobbies, brand-name anything over the generic, gifts, new clothes beyond basics, and the coffee on the way to work.

A lot of people feel guilty about the wants category. Do not. The whole point of the 50/30/20 rule is that wants are budgeted for. You are allowed to spend on them. You just cannot spend more than 30% of your after-tax income on them without blowing up the math.

20% — Savings and Debt Repayment

This is the category that builds your future. It covers contributions to an emergency fund, retirement accounts (401(k), IRA, RRSP, TFSA), investment accounts, and any debt payments above the minimum — the extra $200 you throw at a credit card, not the minimum payment that goes in the needs bucket.

Within the 20%, most financial planners suggest a priority order: first build a $1,000 starter emergency fund, then pay off any debt with an interest rate above 7-8%, then build a full three-to-six-month emergency fund, then ramp up retirement contributions to capture any employer match, then invest beyond that.

How to Apply the 50/30/20 Rule to Your Income

Featured Snippet Target: To apply the 50/30/20 rule, start with your monthly after-tax income (take-home pay). Multiply by 0.50 for your needs budget, 0.30 for wants, and 0.20 for savings. For example, $5,000 take-home becomes $2,500 needs, $1,500 wants, $1,000 savings.

Here is the step-by-step process.

-

Calculate your monthly after-tax income. This is what lands in your bank account after federal tax, state or provincial tax, Social Security or CPP, Medicare or EI, and any other mandatory deductions. Not your gross salary. If your paycheck varies, average the last three months.

-

Subtract your pre-tax contributions correctly. If you already have 401(k) or RRSP contributions coming out of your paycheck before you see the money, add them back to your take-home for this calculation, because those are your 20% bucket already working. Otherwise you will double-count them.

-

Multiply your adjusted take-home by 0.50, 0.30, and 0.20. These are your monthly targets.

-

Pull three months of transactions from your bank and credit cards. Categorize each into needs, wants, or savings. Be honest.

-

Compare your actuals to your targets. The gap is your blueprint.

Real Examples Across Income Levels

Example 1: $3,000 Monthly After-Tax Income

-

Needs: $1,500 — this is tight in most urban areas. You are looking at shared housing, a used reliable car or transit, a strict grocery budget around $300-400.

-

Wants: $900 — room for a few meals out, one streaming service, a modest hobby budget.

-

Savings: $600 — start with $100 to a starter emergency fund, rest toward high-interest debt or retirement match.

Example 2: $5,500 Monthly After-Tax Income

-

Needs: $2,750 — rent or mortgage around $1,500, utilities $200, groceries $500, transportation $350, minimums $200.

-

Wants: $1,650 — dining, subscriptions, travel fund, shopping, entertainment.

-

Savings: $1,100 — this is where real wealth starts to build. A full emergency fund within 12-18 months, retirement contributions, and the beginning of an investment portfolio.

Example 3: $9,000 Monthly After-Tax Income

-

Needs: $4,500 — but most people at this income should be well under 50% for needs. The rule becomes a ceiling, not a target.

-

Wants: $2,700 — lifestyle creep territory. The danger here is spending the full amount just because the rule allows it.

-

Savings: $1,800 minimum — at this income, the smart move is usually closer to 30% savings. The rule is a floor to beat, not a goal to hit.

Common Mistakes to Avoid

Mistake 1: Using gross income instead of net

This is the number-one error. Your gross salary is a fiction that exists only on offer letters. The 50/30/20 rule uses take-home pay, because you cannot spend money the government already took.

Mistake 2: Putting everything you 'need to' pay into needs

Your Netflix subscription is not a need because you need to relax. Your gym membership is not a need because you need to be healthy. Be ruthless here. If the charge stopping would not cause a crisis within a month, it is a want.

Mistake 3: Treating minimum debt payments and extra debt payments the same

Minimum payments go in the 50% needs bucket because missing them tanks your credit. Any extra you throw at debt — the portion above the minimum — is wealth-building and belongs in the 20% bucket.

Mistake 4: Budgeting monthly for expenses that are not monthly

Car insurance renewals, property tax, holiday gifts, annual subscriptions. Divide these by 12 and set aside a twelfth each month in a sinking fund, categorized wherever the expense lives. Otherwise a big December bill blows up your whole year.

Mistake 5: Giving up after one bad month

Nobody hits the targets the first month. The point is the direction, not perfection. If your first honest count shows 60/35/5, that is data, not failure. Fix one line at a time.

When the 50/30/20 Rule Does Not Work

The rule breaks in two situations, and knowing this matters.

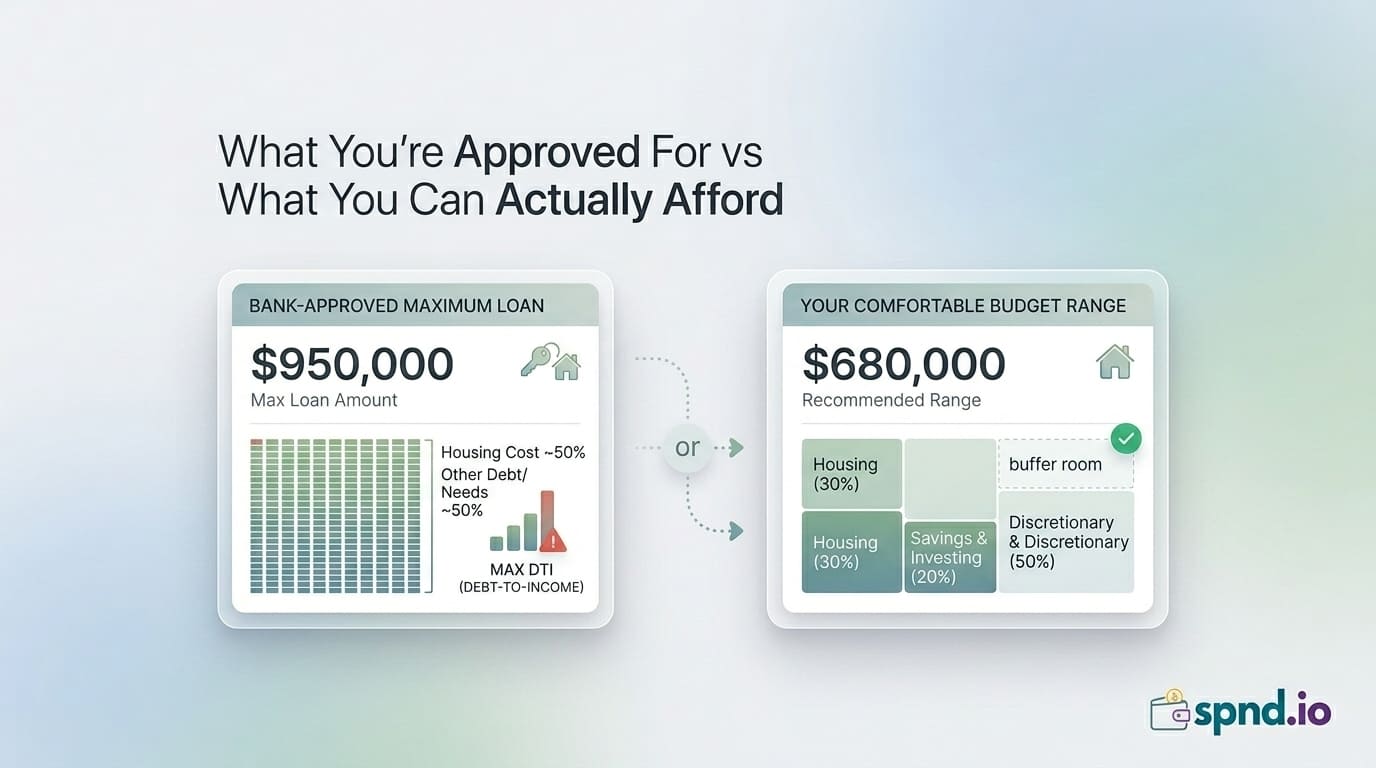

First, in high cost-of-living areas with modest incomes. If you live in Toronto, Vancouver, New York, San Francisco, or another top-five housing market, rent alone can hit 40-50% of take-home. That leaves no room for the rest of needs, never mind wants and savings. The 50/30/20 rule is useful here only as a goal to work toward — via raising income, moving, or finding housemates — not a rule you can apply tomorrow.

Second, when you are paying down aggressive debt. If you have $20,000 in credit card debt at 22%, the math of splitting neatly does not work. The right play is often closer to 50/20/30 or even 50/10/40, where you treat debt elimination like a house on fire until the balance is gone. Then you return to standard 50/30/20.

In both cases, the rule is still a benchmark. Knowing you are at 65/25/10 instead of 50/30/20 tells you exactly what lever to move and by how much.

50/30/20 vs Other Budgeting Methods

The 50/30/20 rule is not the only game in town. Quick comparison:

-

Zero-based budgeting gives every dollar a job before the month starts. More control, more admin. Best if you like spreadsheets and have irregular spending.

-

Pay-yourself-first automates the savings portion (usually 15-20%) on payday and lets you spend the rest however. Simpler than 50/30/20 but less structure on the spending side.

-

Envelope or cash stuffing method uses physical or digital envelopes for each category. Great for overspenders but clunky in a digital-payment world.

-

70/20/10 (70% needs and wants combined, 20% savings, 10% debt or giving) is even simpler than 50/30/20 but offers less visibility into the needs-versus-wants split where most lifestyle creep hides.

For most people starting out, the 50/30/20 rule is the best balance of structure and livability. You can always graduate to zero-based once you know your numbers.

How to Make the 50/30/20 Rule Stick

Knowing the rule is easy. Living it takes three habits.

-

Automate the 20% first. On payday, transfer your savings portion into a separate account before you can spend it. Every financial planner agrees on this one move.

-

Use separate accounts for needs and wants. Even a simple two-account setup (one for bills, one for spending) makes overspending on wants physically obvious. You cannot overspend what is not there.

-

Review monthly, not daily. Daily tracking is how people burn out. A 20-minute check-in once a month, comparing actuals to the three buckets, is enough.

The rule is not about restriction. It is about making sure today's spending does not starve tomorrow's freedom. Get the split roughly right for six months in a row and you will have built the single most powerful financial habit there is.

Frequently Asked Questions

Is the 50/30/20 rule based on gross or net income?

Net. Use your after-tax take-home pay. Some versions of the rule use gross income, but the original Warren framework and virtually every modern financial planner uses net, because that is the money you actually control.

Does the 50/30/20 rule work if I have student loans?

Yes. Minimum student loan payments go in the 50% needs bucket (they are non-negotiable). Any aggressive payoff above the minimum goes in the 20% savings and debt bucket. If your loans are crushing, temporarily skew toward debt payoff until you are through the worst of it.

Does 401(k) or RRSP pre-tax contribution count in the 20%?

Yes. If your retirement contribution comes out before taxes, it is already your 20% (or part of it) doing its job. Just make sure you add it back when calculating your true effective take-home for the formula, so you do not double-count.

Is the 50/30/20 rule good for beginners?

It is arguably the best beginner budget that exists. It gives you structure without demanding obsessive tracking. If you are new to budgeting and you pick one system, pick this one.

The 50/30/20 rule only works if you know your real take-home pay and can see your spending against the three buckets. Use the spnd.io Budget Planner to set your targets, and the Cashflow Planner to track every week. Both are free and require no account.