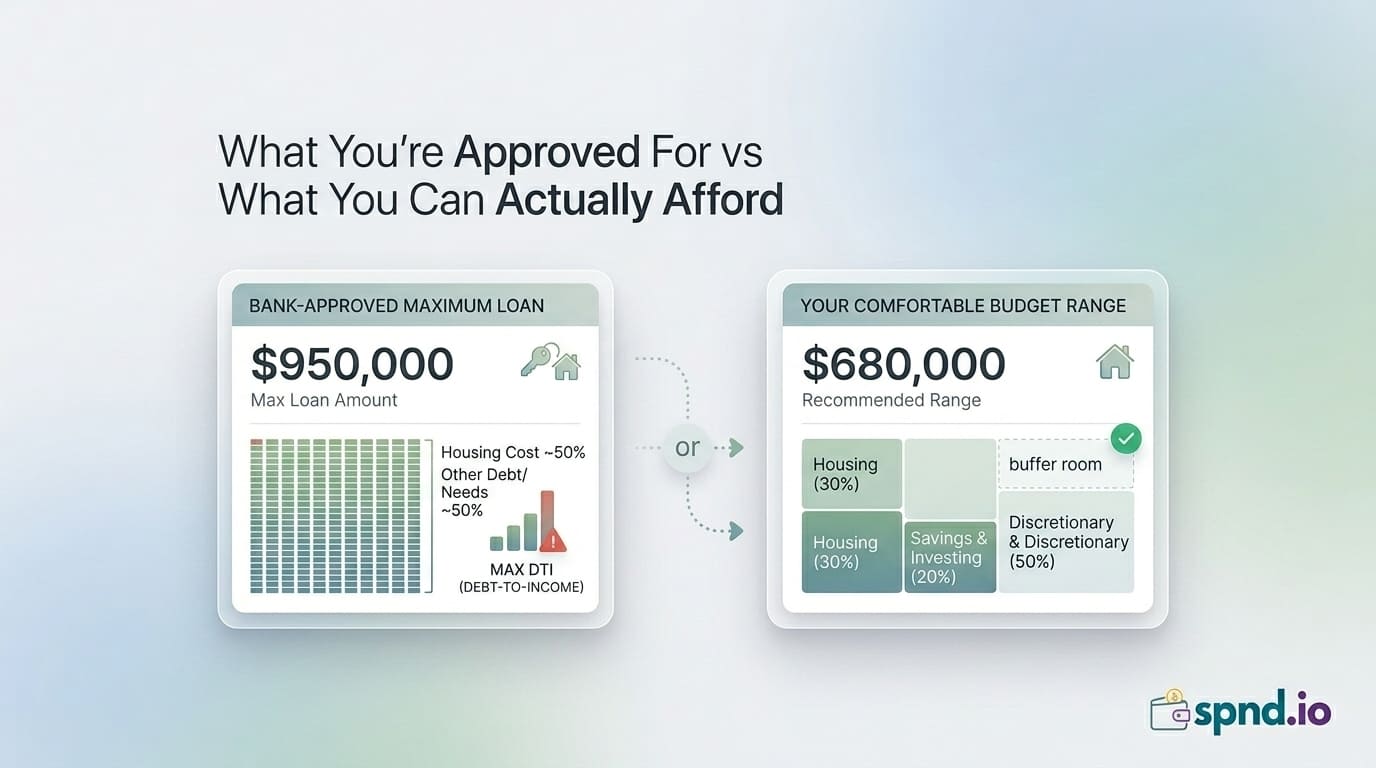

The 50/30/20 rule is a straightforward budgeting method that allocates your after-tax income into three buckets:

- 50% for Needs: Essential expenses like rent, utilities, groceries, transportation, and minimum debt payments.

- 30% for Wants: Non-essential spending like dining out, entertainment, hobbies, or that daily latte.

- 20% for Savings and Debt: Extra debt payments (beyond the minimum), emergency fund contributions, retirement savings, or investments.

For example, if your monthly take-home pay is $4,000:

- $2,000 (50%) goes to needs.

- $1,200 (30%) covers wants.

- $800 (20%) builds your future through savings or debt reduction.

Why the 50/30/20 Rule Works

Unlike restrictive budgets that track every penny, this rule offers balance. It ensures your essentials are covered, gives you room to enjoy life, and forces you to prioritize financial security — all without feeling like a chore. It's flexible enough to adapt to your income and lifestyle, yet structured enough to curb overspending. Here's how it tackles those costly habits:

- Reins in Wants: That $1,200 "wants" budget forces you to choose between daily lattes, takeout, or subscriptions — cutting mindless splurges.

- Boosts Savings: The 20% bucket turns wasted money (like $730 on bottled water) into an emergency fund or investment growth.

- Covers Needs Smarter: By capping needs at 50%, you're motivated to reduce energy waste or negotiate bills.

Applying the Rule to Break Bad Habits

Let's see it in action. Imagine you cut coffee ($1,300/year), lunch ($3,120/year), and subscriptions ($600/year) by adopting the fixes above. That's $5,020 saved annually. With the 50/30/20 rule:

- Redirect $2,510 (50%) to needs — like a lower grocery bill via meal prep.

- Keep $1,506 (30%) for guilt-free wants, like a weekend outing.

- Save or invest $1,004 (20%) — enough to grow into $12,000+ over a decade at a 7% return.

Repeat this for other habits, and the savings multiply. The rule doesn't just stop the bleeding; it builds wealth.

Getting Started

- Calculate Your Income: Use your after-tax monthly pay.

- List Your Expenses: Sort them into needs, wants, and savings/debt.

- Adjust: If your "wants" exceed 30%, target habits like impulse buys or eating out. If savings lag, cut bottled water or energy waste.

- Track Monthly: Use a simple spreadsheet or app to stay on course.

The Bottom Line

Your daily habits might be costing you thousands, but they don't have to. The 50/30/20 rule offers a clear path to break the cycle — balancing today's enjoyment with tomorrow's security. Start small. Pick one habit to ditch this week, apply the rule, and watch your savings grow. Over time, those thousands can become yours again — to spend, save, or invest as you see fit.