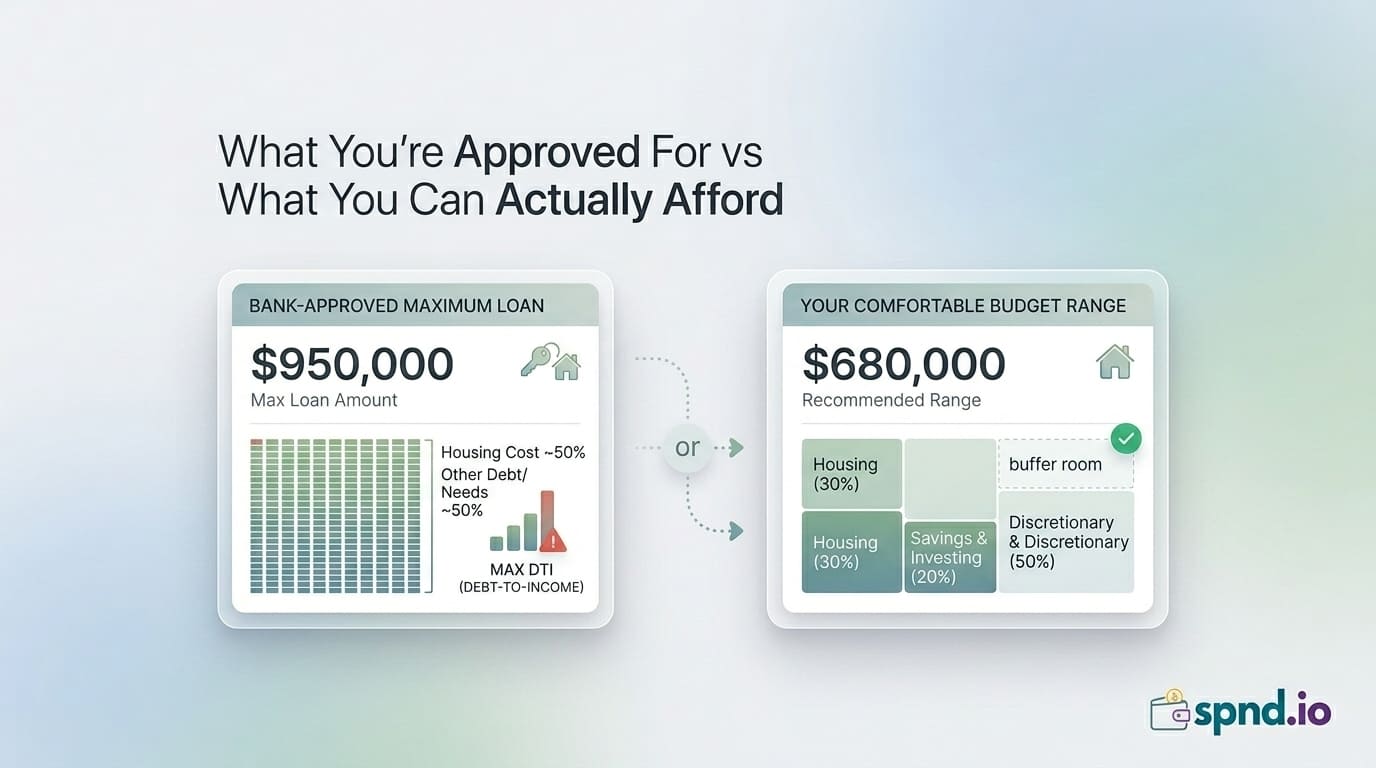

What a lender says you can afford and what you can actually afford are often wildly different numbers. Lenders work off your gross income and focus on whether you will default — your lifestyle, savings goals, and retirement plans are not their problem. If you buy at the top of what a lender approves, you are usually buying more house than your actual life can support.

This guide walks through the math lenders use, the honest math you should use, and how to arrive at a purchase price that leaves room for the rest of your financial goals.

What Lenders Will Approve You For

Most mortgage lenders use two debt-to-income (DTI) ratios.

Front-end DTI: 28% of gross income

Total monthly housing cost (PITI — Principal, Interest, Taxes, Insurance) should not exceed 28% of gross monthly income. For a household earning $120,000 gross ($10,000/month), that is a housing ceiling of $2,800/month.

Back-end DTI: 36-43% total debt

All monthly debt payments combined — housing, auto, student loans, credit card minimums — should not exceed 36% for conventional lending, 43% for most FHA loans, up to 50% for some flexible programs. On $10,000 gross monthly income, that is $3,600-$4,300 total debt payments.

What this approves

A household with $120,000 gross income, $400/month car payment, $300/month student loan, and no other debt could be approved for housing costs up to $2,900-$3,400/month depending on the lender. At 7% interest, 20% down, 30-year term, that supports roughly a $430,000-$510,000 purchase price.

Why Those Numbers Are Too High for Most People

The lender's formula is built on the assumption that you do nothing else with your money. No retirement contributions. No emergency fund. No kids' education savings. No travel. No eating out. No savings toward unexpected expenses. If you actually try to live the life most people want, 28% front-end DTI is too much house for too little room.

Consider the math on $10,000 gross monthly:

-

Gross: $10,000

-

Taxes (federal + state + FICA average): ~$2,500

-

Net (take-home): ~$7,500

-

Lender-approved housing at 28% gross: $2,800

-

Percent of net spent on housing: 37%

37% of take-home on housing leaves 63% — $4,700 — for everything else: food, car, utilities, insurance, retirement, emergency savings, discretionary spending. It is possible. It is not comfortable, and it is certainly not the path to wealth-building.

The 25% of Net Rule

A more honest rule: keep total housing costs (PITI + HOA if applicable + monthly average of repairs) below 25% of take-home pay.

Same $10,000 gross example

-

Take-home: $7,500/month

-

25% rule housing ceiling: $1,875/month

-

Lender's 28% gross ceiling: $2,800/month

-

Difference: $925/month = ~$137,000 less house

That $925/month is what makes the difference between a mortgage that smothers your other goals and a mortgage that fits alongside them.

Total Monthly Cost, Not Just the Payment

The biggest mistake buyers make is only counting principal and interest. Total monthly housing cost includes all of:

-

Principal and interest on the mortgage

-

Property taxes (typically 1-2% of home value per year, divided by 12)

-

Homeowner's insurance (typically $1,000-$3,000/year)

-

HOA or condo fees if applicable ($200-$800/month)

-

Private Mortgage Insurance if you put less than 20% down (0.5-1.5% of loan annually)

-

Budgeted reserve for repairs and maintenance (1% of home value per year, divided by 12)

On a $400,000 home with $320,000 mortgage at 7%, the principal and interest are about $2,130/month. But the actual total monthly cost is closer to $2,900 once you add taxes, insurance, PMI if applicable, and maintenance reserve.

The Maintenance Reserve Nobody Talks About

First-time buyers are often shocked by maintenance costs. The rough rule: 1% of home value per year, averaged across decades. On a $400,000 home, that is $4,000/year or $333/month — all the minor repairs, appliance replacements, paint, water heater, occasional big-ticket items like roofs and HVAC.

Some years this is $500. Other years it is $12,000 when the furnace dies the same week the roof starts leaking. The only way to not be blindsided is to treat the reserve as a non-optional line item in your monthly budget, funded into a dedicated sinking fund.

Down Payment Considerations

The 20% down myth

20% down is the number that avoids Private Mortgage Insurance (PMI). It is not a rule that you must put 20% down to buy a house. Conventional loans go as low as 3% down, FHA loans as low as 3.5%, VA loans at 0% for qualifying veterans.

PMI for low-down-payment buyers is typically 0.5-1.5% of the loan amount annually. On a $400,000 loan, that is $170-$500/month. Expensive, but not the deal-breaker it gets made out to be — especially if waiting to save 20% means paying another 3-5 years of rent on top of the time value of home appreciation.

The 'don't drain your emergency fund' rule

After closing, you should still have: 3-6 months of essential expenses in emergency savings, $5,000-$15,000 in a house-specific reserve for immediate repairs and move-in costs, retirement contributions continuing. If buying the house means zero savings on closing day, you are buying a very expensive way to be broke.

Interest Rates Matter More Than Price (Usually)

A 1% change in mortgage rates changes what you can afford by about 10%. Quick comparison on the same $400,000 purchase with 20% down:

-

5% rate: principal and interest ~$1,720/month

-

6% rate: ~$1,920/month (+$200)

-

7% rate: ~$2,130/month (+$410 vs 5%)

-

8% rate: ~$2,350/month (+$630 vs 5%)

Over 30 years, the difference between a 5% rate and a 7% rate on the same home is $147,000 in extra interest paid. Shopping lenders, improving your credit score before applying, and sometimes waiting for a better rate environment can matter more than squeezing out a slightly lower purchase price.

The Stress Test: Can You Afford It If Life Changes?

Before finalizing a mortgage amount, run your numbers through three stress scenarios:

Scenario 1: One income lost for 6 months

Can the remaining household income cover the mortgage plus essentials? If not, the purchase is fragile.

Scenario 2: Major unexpected expense

A $15,000 medical bill, a $10,000 car replacement, a $6,000 HVAC failure. Do you have the reserves to handle it without putting it on a credit card?

Scenario 3: Rate adjustment (if on variable rate)

If your rate adjusts up by 2 percentage points, can you still afford the payment? For fixed-rate borrowers in the US this is moot, but Canadians who typically renew every 5 years need to stress-test a renewal at 2-3% higher.

When to Buy Less Than You Qualify For

Strong signals that you should buy below your approved maximum:

-

You plan to have kids in the next 5 years (costs go up, one income may drop)

-

You are behind on retirement savings for your age

-

Your income is variable or your industry is unstable

-

You have aggressive other goals (education, business, early retirement)

-

You value flexibility to travel, take sabbaticals, or change careers

Being house-poor — technically a homeowner but spending all disposable income on housing — is one of the most common regrets in personal finance. The house does not get appreciably better as you stretch; the rest of your life gets appreciably worse.

Honest Affordability Formula

A realistic framework:

-

Calculate take-home pay after all taxes and pre-tax deductions

-

Target total housing cost at 25% of take-home (28% absolute ceiling for most buyers)

-

Work backward: 25% of take-home = max total housing cost. Subtract estimated taxes, insurance, and maintenance reserve. What remains is your max principal + interest.

-

At current rates and down payment amount, what purchase price gives that principal + interest? That is your honest maximum.

-

Buy at or below this number

This typically produces a number 15-25% lower than what a lender will approve. That 15-25% is not lost buying power — it is the room for the rest of your life to exist.

See the real payment numbers for any home price, down payment, and rate combination with the free Mortgage Calculator on spnd.io. Pair it with the Net Income Calculator to see what actually fits your take-home pay — not just what a lender will approve.