Budgeting advice is frustrating because every method sounds like it was invented by someone with a personality completely unlike yours. The envelope method assumes you love physical ritual. Zero-based budgeting assumes you love spreadsheets. The 50/30/20 rule assumes you like round numbers more than precision.

None of these are wrong. They are tools, and the right one depends on how your brain works and what financial situation you are actually in. This guide compares the five most popular systems — with honest downsides — so you can pick the one that will still exist in six months.

Quick Comparison

-

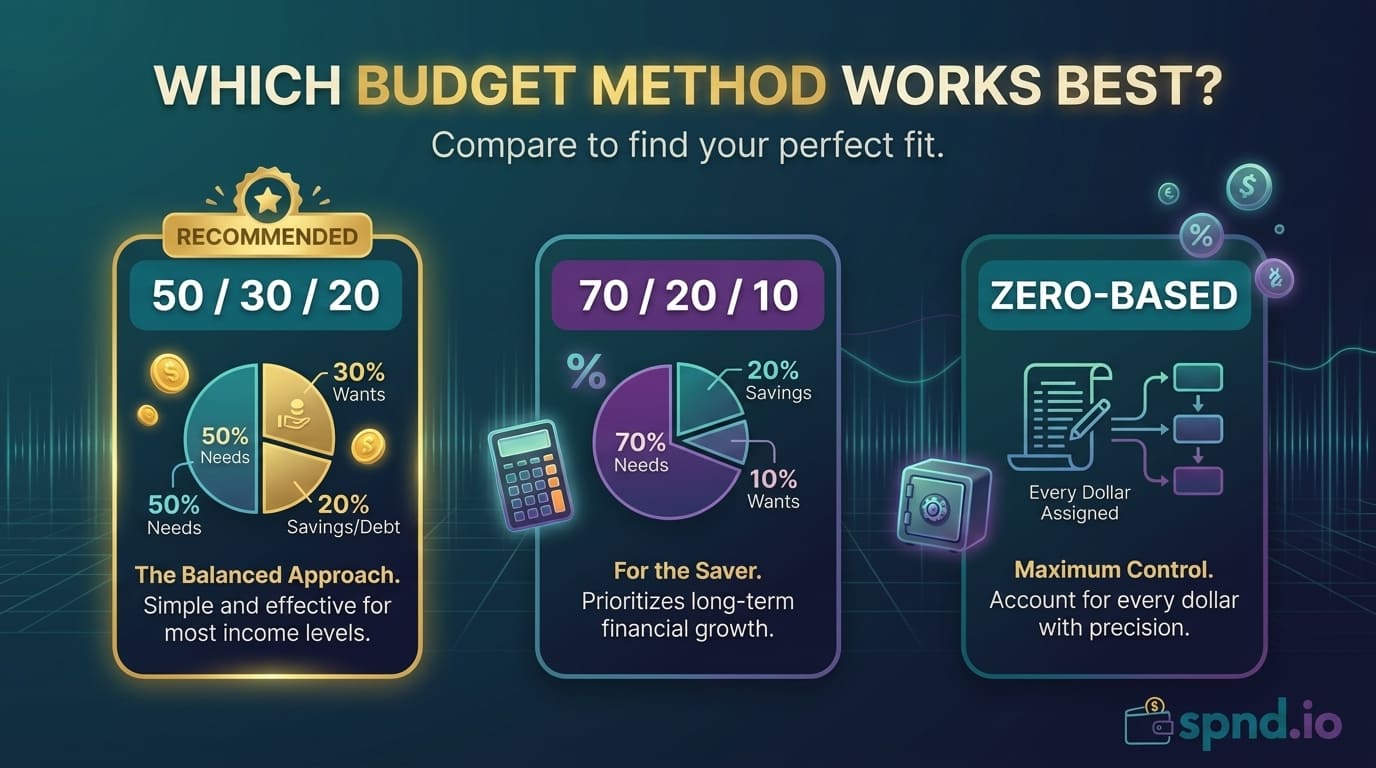

50/30/20 — Three buckets (needs/wants/savings). Simple, flexible, best for beginners.

-

70/20/10 — Even simpler three buckets. Works in tight situations where 20% saving is unrealistic.

-

Zero-based — Every dollar has a job before the month starts. Most control, most work.

-

Pay-yourself-first — Automate savings, spend what is left however. Minimal tracking.

-

Envelope / cash stuffing — Cash or digital envelopes per category. Best for impulse spenders.

The 50/30/20 Rule

How it works

Divide your after-tax income into three buckets: 50% for needs, 30% for wants, 20% for savings and debt repayment above the minimum.

Who it works for

-

Beginners who have never budgeted before

-

People with steady paychecks

-

Anyone who has tried a detailed budget and quit within three weeks

-

Middle-income earners in mid-cost areas

Strengths

-

Impossible to forget — three numbers fit in your head

-

Forces a savings target, not a leftover

-

Gives you permission to spend on wants without guilt

-

Scales across income levels

Weaknesses

-

Breaks down when housing alone eats 40%+ of your income

-

Does not tell you how to prioritize within the savings bucket

-

The needs/wants line is judgment-dependent and can get fuzzy

The 70/20/10 Rule

How it works

Divide after-tax income into: 70% for all living expenses (needs AND wants combined), 20% for savings, 10% for debt repayment or charitable giving. Some versions flip the last two or combine them into one 'financial goals' bucket.

Who it works for

-

People in high cost-of-living cities where 50% for needs is impossible

-

Anyone juggling aggressive debt who wants a separate debt line

-

People who find even three categories too many and prefer one lifestyle bucket

Strengths

-

More realistic for tight budgets

-

Separates debt from savings so you see progress on both

-

Simpler than 50/30/20 — you do not have to argue about what is a need

Weaknesses

-

Combining needs and wants hides lifestyle creep

-

20% savings is still ambitious and can feel like a ceiling, not a floor

-

Less structure means less protection against overspending

Zero-Based Budgeting

How it works

Before the month starts, you assign every dollar of expected income to a specific category — rent, groceries, gas, fun money, savings, whatever. Income minus assignments should equal zero. If you have 'leftover' money, you have not been specific enough. Popularized by YNAB (You Need A Budget) and Dave Ramsey.

Who it works for

-

People who enjoy control and detail

-

Self-employed or freelancers with irregular income

-

Anyone digging out of serious debt who needs maximum intentionality

-

Couples who want a shared, transparent system

Strengths

-

Maximum control and visibility

-

Builds serious financial literacy — you cannot fake it

-

Handles irregular income better than any other method

-

Catches problems before they happen

Weaknesses

-

Requires 2-5 hours of setup, then 30-60 minutes per week

-

Hard to sustain without an app or dedicated spreadsheet

-

High burnout rate among people who are not naturally detail-oriented

Pay-Yourself-First

How it works

On payday, automate the transfer of a fixed percentage (usually 15-25%) into savings and retirement accounts before you see the money. Then spend the rest however you want for the month, no category tracking required. The rule was popularized by The Richest Man in Babylon and George Clason's 'one-tenth' principle.

Who it works for

-

People who hate tracking but like automation

-

Higher earners who already live below their means

-

People who have tried detailed budgets and quit

Strengths

-

Set it up once, ignore it forever

-

Zero cognitive load

-

Removes willpower from the equation

Weaknesses

-

No visibility into how you are actually spending the rest

-

Lifestyle creep can consume the 'rest' over time

-

Does not help you pay down debt aggressively — savings rate stays fixed

Envelope / Cash Stuffing Method

How it works

Put cash (or digital cash equivalents) into labeled envelopes at the start of each month: groceries, gas, dining out, entertainment, etc. When an envelope is empty, you are done spending in that category for the month. Traditionally done with physical cash. Modern 'cash stuffing' uses either physical envelopes or sub-account banking.

Who it works for

-

Chronic overspenders who cannot self-limit

-

Anyone who feels disconnected from their spending when it is digital

-

People recovering from addiction to credit

-

Visual learners who need tactile feedback

Strengths

-

Physical constraint prevents overspending

-

Makes money feel real

-

Studies suggest people spend 12-18% less when using cash

Weaknesses

-

Impractical for most modern bills (rent, utilities, subscriptions)

-

Cash is a security risk — you lose an envelope, you lose the money

-

Digital cash stuffing requires banks that support sub-accounts

-

Time-consuming to maintain

How to Pick: A Decision Framework

Pick 50/30/20 if

-

You have never budgeted and want to start

-

Your income is steady

-

You want to save seriously but not obsessively

Pick 70/20/10 if

-

You live somewhere expensive where 50% for needs is unrealistic

-

You have both savings goals AND aggressive debt

-

You want structure but not as much as 50/30/20

Pick zero-based if

-

You love detail and control

-

Your income is irregular (freelance, commission, self-employed)

-

You are digging out of serious debt

-

You are willing to spend 30-60 minutes per week on it

Pick pay-yourself-first if

-

You have tried detailed budgets and quit

-

You earn enough to save meaningfully while ignoring spending

-

You want zero ongoing effort

Pick envelope / cash stuffing if

-

You consistently overspend on specific categories

-

You respond to physical or visual constraints

-

You are willing to deal with cash or sub-accounts for daily spending

The Honest Truth: The Best Budget Is The One You Do

A zero-based budget you quit in 30 days is worse than a 50/30/20 rule you follow loosely for five years. A perfect envelope system you cannot maintain is worse than a pay-yourself-first automation that runs on its own.

If you have never budgeted, start with 50/30/20 — it has the best beginner completion rate. If you have tried that and found it too loose, graduate to zero-based. If you found it too tight, drop to pay-yourself-first and rebuild discipline slowly. The methods are not religions. Switch when your life changes.

The one common thread across all five: they work because they impose structure you would not otherwise impose on yourself. Any structure is better than none. Pick one, start this week, adjust after three months.

Whichever method you pick, you still need to know your numbers. The free spnd.io Budget Planner and Cashflow Planner work with any of these frameworks — plug in your income and expenses, and the tools do the math.