If you have read five articles about the 50/30/20 budget rule, you have probably read three different answers to this question. One site tells you gross. Another tells you net. A third tells you it does not matter. The third one is wrong.

It matters a lot. Using gross instead of net can overstate your budget by $1,000 or more every month. This post settles the question, explains why the answer is net, and walks you through exactly how to calculate the right number for your situation — whether you are in the US or Canada, salaried or hourly, employed or self-employed.

The Short Answer: Use Net Income

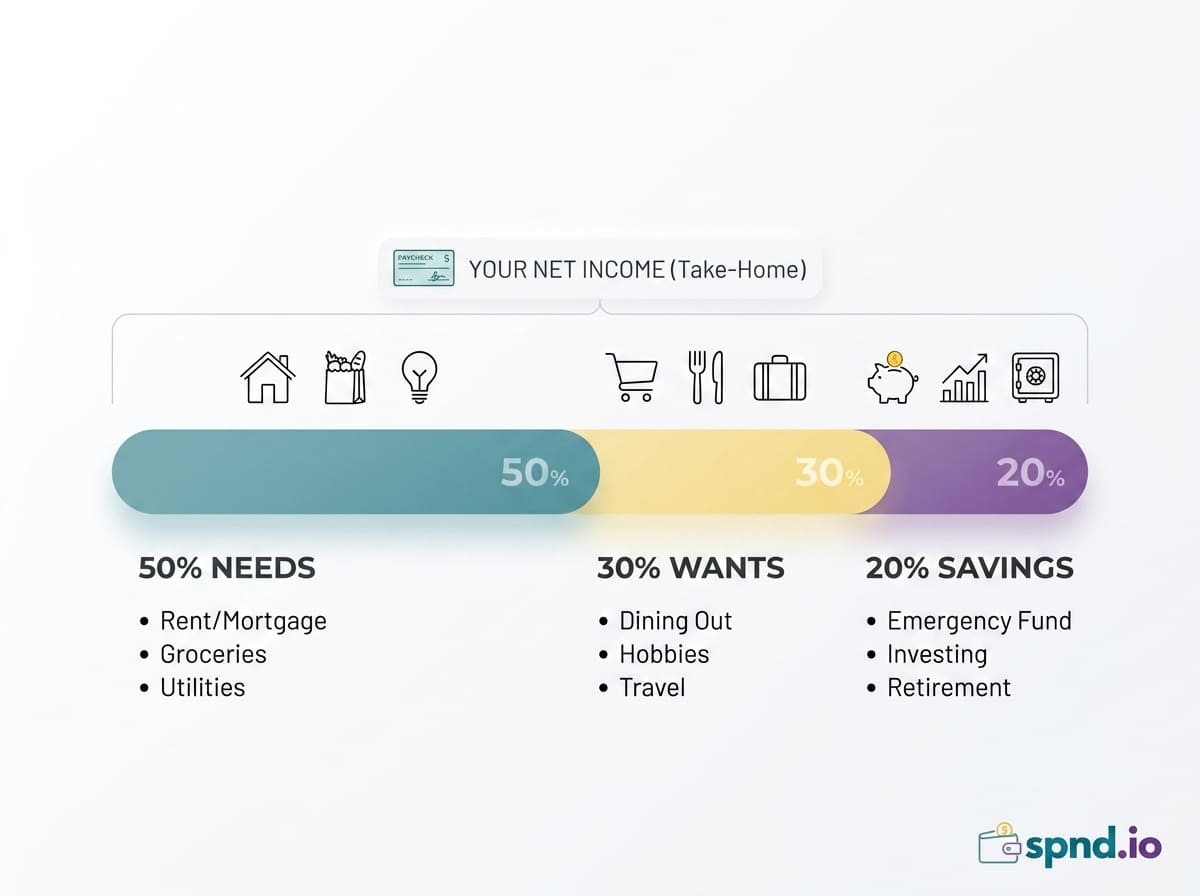

The 50/30/20 rule uses net income — your take-home pay after taxes and mandatory deductions. This is the number that actually lands in your bank account on payday. It is the money you can spend, save, or invest. It is your real financial reality.

The confusion exists because Elizabeth Warren's original book, All Your Worth, used 'after-tax income' throughout. Some later summaries translated that as 'gross income' when simplifying for blog posts, and the mistake stuck. The original framework was always based on what you actually bring home.

Why Using Gross Income Wrecks Your Budget

Imagine a $75,000 salary. That is your gross. After federal tax, state tax, Social Security, and Medicare, your take-home in most US states is closer to $57,000 — about 76% of gross. In Canada with similar income and provincial taxes, the gap is often even larger.

Apply the 50/30/20 rule to gross income and your monthly targets become:

-

Needs: $3,125

-

Wants: $1,875

-

Savings: $1,250

But you only have $4,750 per month to work with, not $6,250. So your real targets should be:

-

Needs: $2,375

-

Wants: $1,425

-

Savings: $950

The difference is roughly $1,500 of phantom money every month. Follow the gross version and you will overspend, underinvest, and wonder why you can never catch up. This is the single most common reason people say 'the 50/30/20 rule does not work for me.' It is working. You are just using the wrong number.

What Counts as Net Income

Your net income is your gross income minus:

-

Federal income tax

-

State or provincial income tax (where applicable)

-

Social Security in the US / CPP (Canada Pension Plan) in Canada

-

Medicare in the US / EI (Employment Insurance) in Canada

-

Any other mandatory deductions like state disability insurance

Pre-tax retirement contributions (401(k), 403(b), or RRSP through payroll) are a special case covered in the next section.

The 401(k) and RRSP Complication

Here is where most people get tripped up. If your employer deducts a 401(k) or RRSP contribution from your paycheck before taxes, that money never shows up in your take-home. But it absolutely counts as part of your 20% savings bucket — it is literally retirement savings.

So you have two correct ways to handle it:

Method 1 — Add It Back (Recommended)

Calculate your take-home the way your paycheck shows it, then add your pre-tax retirement contributions back. That gives you your effective after-tax income. Use that for the 50/30/20 split. Your pre-tax contributions then count toward the 20% bucket automatically.

Example: $4,200 take-home + $600 pre-tax 401(k) = $4,800 effective net income. Your targets are $2,400 / $1,440 / $960. Since $600 of the savings bucket is already going to the 401(k) from your paycheck, you only need to save $360 more on your own to hit the full 20%.

Method 2 — Use Straight Take-Home

Use the number in your bank account with no adjustment. Simpler, but you will probably undercount your savings progress because the pre-tax contribution is invisible. This method works fine if you are already contributing aggressively and just want a rough guide for discretionary spending.

How to Calculate Your Net Income Exactly

If You Are Salaried

Look at your most recent pay stub. The 'net pay' or 'take-home' line is your answer. Multiply by the number of pay periods per year (26 for bi-weekly, 24 for semi-monthly, 12 for monthly) and divide by 12 to get monthly net income. If your pay varies slightly period to period, average the last three months.

If You Are Hourly

Pull your last three months of pay stubs. Add up the net pay. Divide by three. That is your monthly net income baseline. If your hours fluctuate significantly, budget conservatively using the lowest of the three months and treat the overages as bonus savings.

If You Are Self-Employed or a Freelancer

This is harder because no one is withholding taxes for you. Start with your gross monthly income, then subtract:

-

Business expenses

-

Estimated taxes — roughly 25-30% of net business income for US self-employed (federal + state + self-employment tax), or 25-33% for Canadian self-employed depending on province

-

Contributions to a SEP-IRA, Solo 401(k), or RRSP if you are using them

What remains is your personal take-home. Use a self-employed calculator for your region to get the exact number, and always set aside the tax portion in a separate account the day you get paid.

Common Net Income Mistakes

Mistake 1: Forgetting health insurance premiums

If your employer deducts health insurance from your paycheck, it is already gone by the time you see your take-home. Do not try to add it back — it is already excluded from net.

Mistake 2: Counting bonus pay as regular income

An annual bonus should not be built into your monthly 50/30/20 math. Treat bonuses as lump-sum savings events. The cleanest approach is to throw 80-90% of any bonus into the 20% bucket and enjoy the rest.

Mistake 3: Using last year's take-home

Raises, tax changes, benefit changes, new deductions, changed filing status — any of these shifts your net. Recalculate every January, and whenever a major life event happens (marriage, kid, new job).

Mistake 4: Not accounting for a spouse's income

If you share finances, use combined household net income for the 50/30/20 split. Doing it separately usually means one person subsidizes the other without either of you realizing it.

Quick Reference: Gross to Net Estimates

As a rough planning estimate before you calculate exactly:

-

US: Net is roughly 70-78% of gross for middle incomes ($50,000-$150,000), depending on your state

-

Canada: Net is roughly 68-76% of gross for middle incomes ($50,000-$150,000), depending on your province

-

Low-tax states (Texas, Florida, Washington) trend to the high end of the US range

-

High-tax provinces (Quebec, Ontario above $100k) trend to the low end of the Canadian range

These are estimates only. Actual numbers depend on filing status, deductions, pre-tax contributions, and dozens of other factors. Do not budget off a rule of thumb when your paycheck can tell you the real answer.

Apply It Now

The reason the 50/30/20 rule feels like magic for some people and a failure for others usually comes down to this single question. Get the input right and the rule suddenly makes sense. Get it wrong and every calculation compounds the error.

Grab your most recent pay stub. Find your net pay. Multiply by your pay frequency. Divide by 12. That number — and nothing else — is what you multiply by 0.50, 0.30, and 0.20. Everything else in your budget flows from this.

Your net income is the only input the 50/30/20 rule needs to work. Use the spnd.io Net Income Calculator to get your exact take-home for the US or Canada in 60 seconds, then plug that number into the Budget Planner to set your three targets.