Budgeting

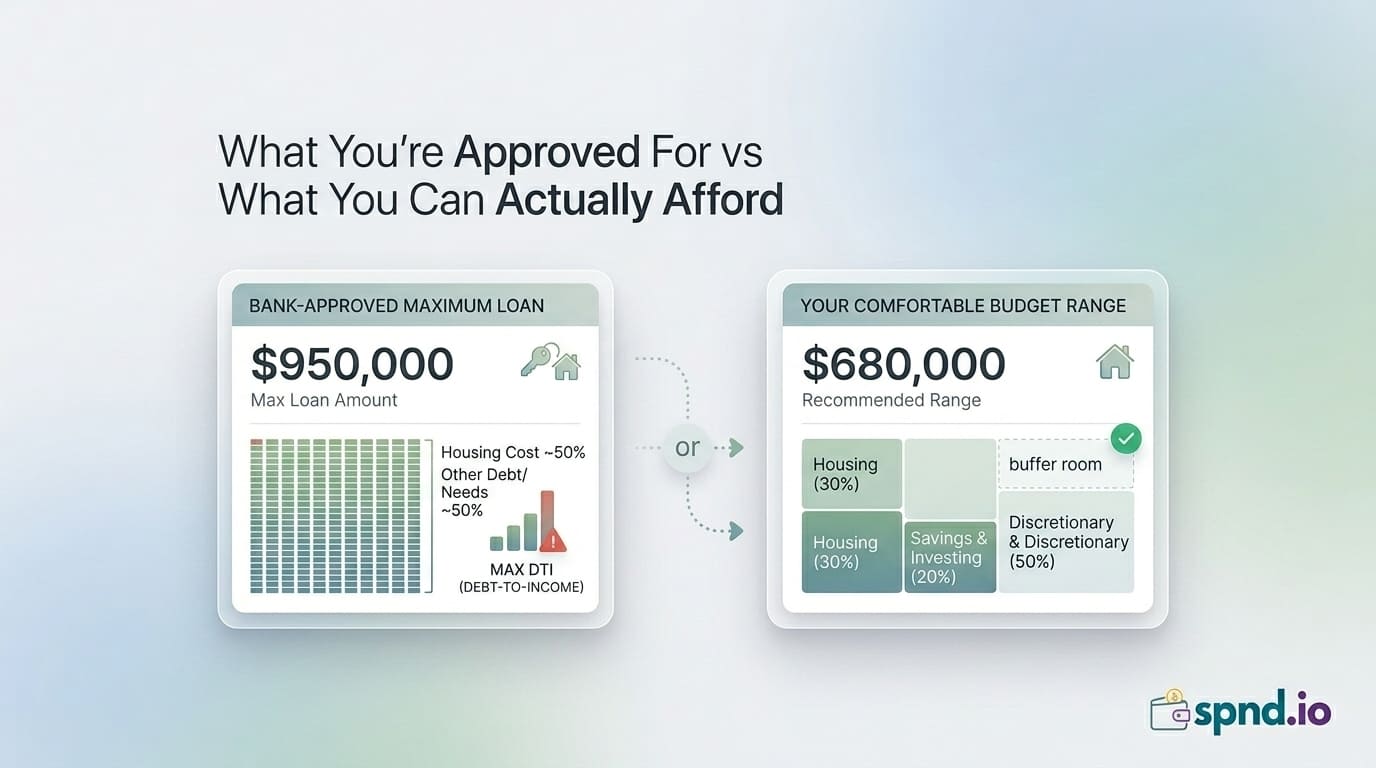

Mortgage Affordability: How Much House Can You Really Buy?

Lenders typically approve mortgages where housing costs stay under 28% of gross monthly income (front-end ratio) and total debt stays under 36-43% (back-end ratio). For real affordability, a stricter rule works better: keep total housing costs under 25% of take-home pay so you have room for savings, emergencies, and the rest of life.

📅 May 12, 2026

·

🕐 3 min read

·

👤