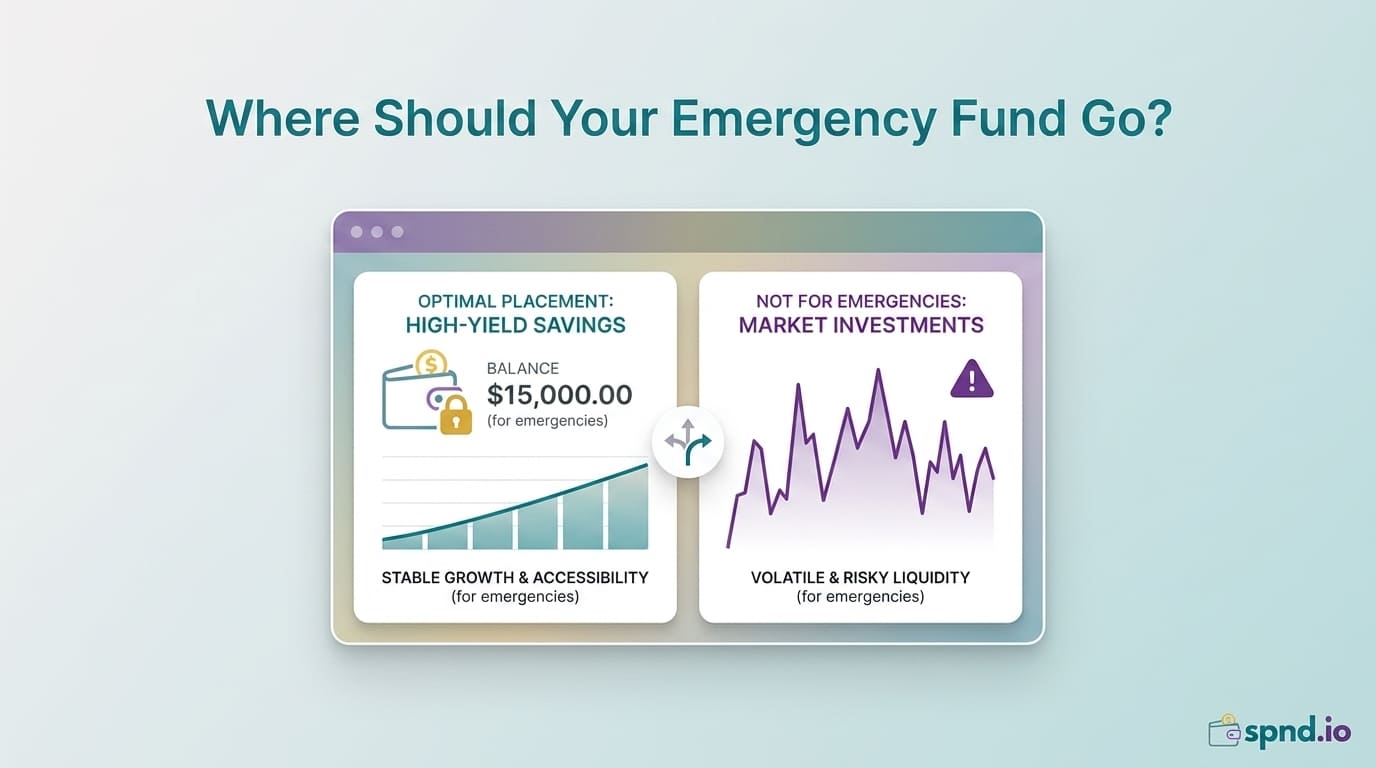

Where you park your emergency fund matters almost as much as having one in the first place. Put it in checking and it earns nothing and gets spent by accident. Put it in a brokerage account and it is vulnerable to market drops at the exact moments you would most need it. Put it in a term deposit and you cannot access it fast enough to help.

This post walks through the right types of accounts for an emergency fund in both the US and Canada, what to look for, and what to avoid. With 2026 high-yield savings rates sitting well above inflation for the first time in years, there is real money left on the table for every month your fund sits in the wrong place.

The Three Rules for Emergency Fund Accounts

-

Immediately liquid — you can access it in under 48 hours without penalty

-

Federally insured — FDIC in the US, CDIC in Canada

-

Safe from market movement — no stocks, crypto, or investment vehicles that can drop 20% at the wrong moment

Any account type meeting all three is fair game. Return rate is a secondary consideration — the fund exists for safety and access, not growth.

Best Options for US Residents

High-Yield Savings Accounts (HYSA)

The default and best choice for most people. Online banks offer 3-5% APY in 2026 with no fees, no minimums, full FDIC insurance, and same-day or next-day transfers to linked checking.

What to look for

-

APY of at least 3.5% (major online banks are typically in this range)

-

No monthly maintenance fee

-

No minimum balance requirement

-

FDIC insured up to $250,000 per depositor

-

Easy electronic transfers to your checking account (2 business days or less)

-

Mobile app for transfers

Money Market Accounts

Similar to HYSA, often with check-writing privileges and slightly higher minimum balance requirements. Yields are typically comparable to HYSA in 2026. Fine choice if you want the check-writing flexibility, but offers no real advantage over a good HYSA for most people.

Treasury Money Market Funds

Available through brokerage accounts (Fidelity, Schwab, Vanguard). Invest in US Treasury bills and offer yields competitive with HYSAs. Not FDIC insured but are considered effectively risk-free because of the US government backing of underlying securities. Good option if you already have a brokerage and want to keep accounts minimal — though technically they fail the FDIC-insured rule, many financial planners consider them safe enough for emergency fund purposes.

Series I Savings Bonds (Tier 2 only)

Inflation-protected government bonds. Rate resets every 6 months. Pros: completely safe, rate keeps pace with inflation. Cons: cannot be sold within the first 12 months, lose 3 months of interest if sold within 5 years. Only appropriate for the 'secondary reserve' (tier 2) of a two-tier emergency fund, not the immediately-accessible portion.

Best Options for Canadian Residents

High-Interest Savings Account (HISA)

The Canadian equivalent of a US HYSA. Online banks like EQ Bank, Simplii, and Tangerine offer 2.5-4% interest in 2026, with no monthly fees, no minimums, and CDIC insurance up to $100,000 per depositor per category.

TFSA High-Interest Savings Account

A HISA held within a TFSA wrapper. Same access and safety as a regular HISA, but interest earned is completely tax-free. For Canadians in any tax bracket, this is usually better than a non-registered HISA — tax-free interest compounds faster, and the contribution room is restored the following year if you make a withdrawal.

Nuance: If you have not maxed your TFSA contribution room, consider whether the emergency fund is the best use of that space. For many people, TFSA room is better used for long-term investments. A non-registered HISA for the emergency fund and TFSA for investments is often the cleaner structure.

Cashable GICs

Short-term GICs (typically 30-90 days) that can be cashed in before maturity without significant penalty. Sometimes offer slightly higher rates than HISAs. Only useful as a tier 2 strategy — not for the immediately-accessible portion of your fund.

What to Avoid

Your regular checking account

Earns 0.0-0.1% APY in virtually all cases. Also psychologically dangerous — money in checking gets spent without deliberate decision. Physical and account separation from daily spending is a feature, not a bug.

Long-term CDs or GICs (terms > 6 months)

Higher yields, but you cannot access the money without a substantial penalty. An emergency that cannot wait 6+ months is exactly the emergency the fund exists for.

Stock market accounts

Index funds, ETFs, individual stocks, robo-advisors. The issue is correlation — job losses, recessions, and medical bankruptcies often coincide with market downturns. You do not want your emergency fund to be 30% smaller in the exact month you lose your job.

Cryptocurrency

Volatility is 10-50x higher than equities. Regulatory risk, custodial risk, exchange failures. Not an emergency fund asset under any interpretation.

Real estate equity

HELOCs are sometimes suggested as an emergency backup. Problem: banks tighten HELOC access precisely when you most need it (during recessions, after job loss, during housing downturns). The access you thought you had evaporates. Not a substitute for liquid cash.

Life insurance cash value

Permanent life insurance policies accumulate cash value that can be borrowed against. But access takes days to weeks, policies have complex rules, and loans from cash value can affect the death benefit. Not a substitute for an actual emergency fund.

The Two-Tier Setup in Practice

For most people, the cleanest structure looks like this:

Tier 1: $1,000-$5,000 in a primary HYSA/HISA

Open an account at a well-known online bank, link it to your checking account, automate a transfer on every payday. This is your immediate access money for small-to-medium emergencies — car repair, urgent travel, small medical bills.

Tier 2: The rest of your target in a separate HYSA/HISA

Ideally at a different bank, or at minimum in a clearly separate account. This is the multi-month reserve for major disruptions. Accessing it should feel like a big deal — that friction is a feature.

Keeping the two tiers in different accounts, even at the same bank, also helps psychologically. You see a clean balance in tier 1 that is 'safe to use without panic.' You see tier 2 and know 'we are not in that territory yet.'

What About Earning More?

Every few months someone in a personal finance forum argues that emergency funds should be invested because the opportunity cost of 3-5% is real. The math:

-

$30,000 emergency fund in HYSA at 4%: $1,200/year in interest

-

$30,000 emergency fund in S&P 500 ETF at 8% average: $2,400/year in returns

-

Difference: $1,200/year

But: the S&P 500 has historically dropped 30-40% in major downturns. If that happens when you need the fund, your $30,000 is now $18,000 at exactly the moment you needed every dollar. The expected return is higher; the expected utility during an actual emergency is significantly worse. The point of the emergency fund is not optimization — it is certainty.

Once you have a full emergency fund, additional savings can go into investment accounts, where they should not need to be touched for years. Do not make the emergency fund do double duty.

Quick Setup Checklist

-

Calculate your essential monthly expenses (not total spending)

-

Decide on your target size (3, 6, 9, or 12 months based on your situation)

-

Open a high-yield savings account at a no-fee online bank — ideally at a different institution than your primary checking

-

Set up an automatic transfer from checking on payday (any amount beats nothing)

-

Do not enable a debit card or checks on this account — friction is a feature

-

Review the account quarterly — switch banks if a better rate becomes available

-

When you hit your target, redirect the automatic transfer to retirement/investments

Browse the spnd.io No-Fee Bank Account Directory to compare high-yield savings accounts across US and Canadian banks side by side — interest rates, minimums, fees, and features in one place. Open the right account once and your emergency fund works while you sleep.