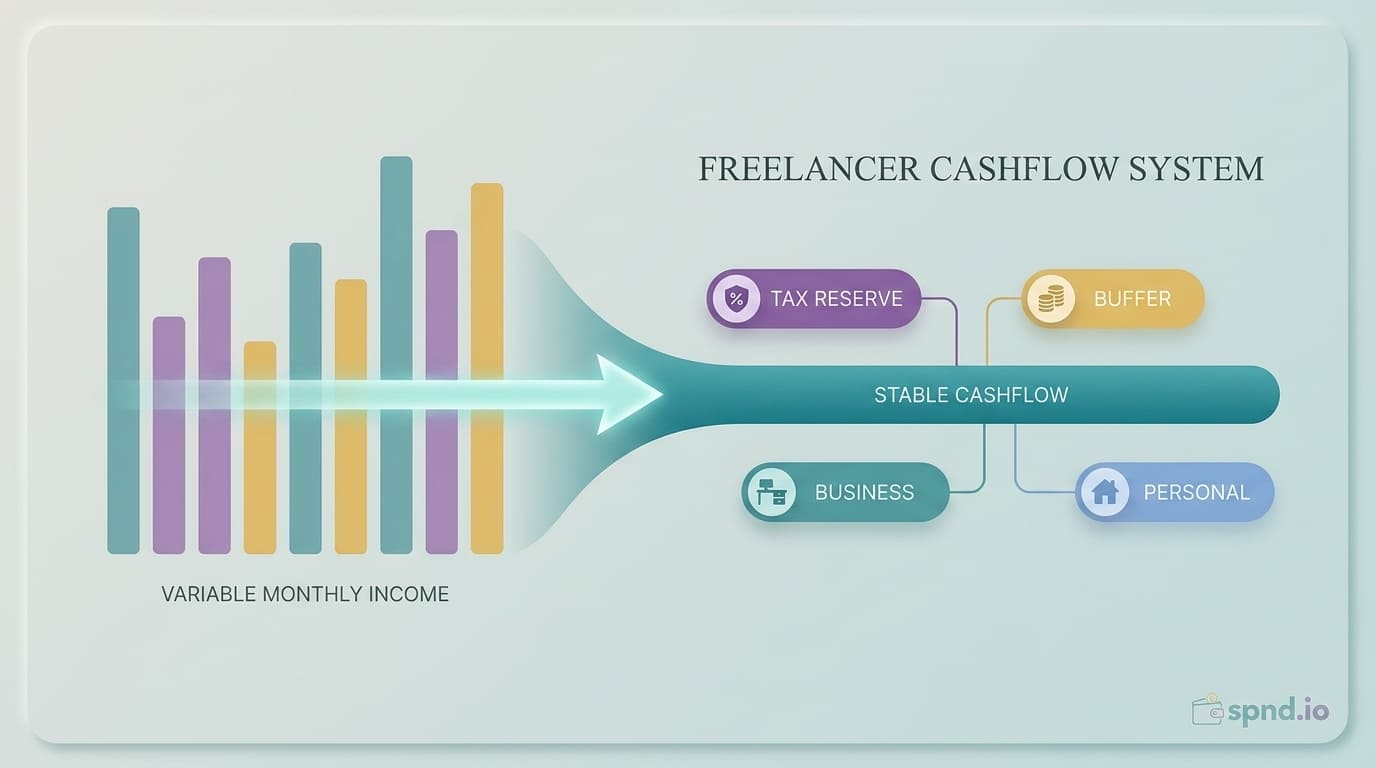

Standard budgeting advice assumes a steady paycheck that lands the same day every two weeks. Freelancers, contractors, commission workers, and small business owners get a different reality: $8,000 one month, $1,400 the next, $4,500 after that, a feast-famine cycle that makes every standard budgeting app feel useless.

The solution is not harder discipline. It is a different structure — one that separates your business income from your personal cashflow with a buffer account in between. This guide walks through that system, plus the tax planning, irregular expenses, and sanity checks that make it actually work.

Why Standard Budgets Fail for Irregular Earners

Most budgeting advice is built on two assumptions: you know your income each month, and you know your expenses each month. Remove the first assumption and the whole system collapses. If $8,000 arrives in March and $1,400 arrives in April, there is no stable percentage to allocate — the 50/30/20 rule cannot tell you whether to live large in March and starve in April, or average somehow.

The fix is not to give up structure. It is to add a buffer between the chaos of business income and the rhythm of personal spending.

The Pay-Yourself-a-Salary System

The core structure has four accounts:

Account 1: Business Checking

Every dollar of business income lands here. Every business expense is paid from here. Never touch it for personal reasons. If you are a sole proprietor, this is psychologically separate rather than legally separate; if you have an LLC or corporation, it is both.

Account 2: Tax Savings

A high-yield savings account linked to your business checking. On every deposit to business checking, immediately transfer 25-30% (US) or 25-33% (Canada, depending on province) to this account. This money is not yours — it belongs to the government and you are just holding it. Never touch it except for quarterly estimated taxes or year-end tax filing.

Account 3: Business Buffer

Another savings account holding 2-3 months of your planned 'salary.' This is the shock absorber. When you have a good month, overflow lands here. When you have a bad month, this account tops up your salary to the normal amount. This is what makes the whole system work — it is the buffer that lets you pay yourself consistently despite inconsistent income.

Account 4: Personal Checking

Receives your 'salary' — a fixed monthly transfer from business checking (or from the buffer when business checking is light). You live off this account the way any salaried person lives off their paycheck. Standard budgeting rules now apply because the income looks steady.

How to Calculate Your Salary Number

Getting the salary amount right is the single most important decision. Too high and you drain the buffer within a few lean months. Too low and you build up unnecessary tension in the business account.

Step 1: Figure out your annual business income (after business expenses)

If you have 12+ months of history, use the trailing 12 months. If you are new, use your best honest estimate on the low side — it is better to pay yourself a modest salary with upward adjustments than to overpay and have to cut. First-year freelancers should estimate conservatively using 60-70% of their 'expected' revenue.

Step 2: Subtract estimated taxes

25-30% for US self-employed (federal, state, self-employment tax). 25-33% for Canadian self-employed depending on province. This is the amount you move to the tax account throughout the year.

Step 3: Subtract retirement contributions

If you are contributing to a SEP-IRA, Solo 401(k), or RRSP from business income, subtract those contributions. These come off the top along with taxes.

Step 4: Divide by 12

What remains is your total annual personal income. Divide by 12 for a monthly salary. Round down to a clean number for consistency.

Example

-

Annual business income after expenses: $90,000

-

Tax reserve (27%): $24,300

-

SEP-IRA contribution (10%): $9,000

-

Available for personal use: $56,700

-

Monthly salary: ~$4,700

You pay yourself $4,700 on the 1st of every month, regardless of whether your business earned $12,000 that month or $900.

Building the Business Buffer

The buffer is what lets the system work when revenue dips. Start at 2 months of salary ($9,400 in the example above), build to 3 months within 6-12 months of starting.

How to build it:

-

On every good month (revenue above average), transfer the overflow to the buffer account first, before considering increases to your salary.

-

On average months, don't touch it.

-

On lean months, pull from the buffer to top up your salary.

Once the buffer is at 3 months of salary, any further overflow can go toward: higher retirement contributions, a personal investment account, or a gradual increase in your salary amount (if you have a year of data showing sustainable revenue growth).

Handling Tax Payments

The tax reserve account is where most freelancers screw up. The two failure modes:

-

Underestimating the reserve and facing a 5-figure tax bill they cannot pay

-

Treating the reserve as 'extra money' and dipping into it for personal expenses

Both are catastrophic. The tax reserve is not yours. Treat it like a customer deposit — handled temporarily, never spent. If your account earns a few dollars of interest, that is yours to keep, but the principal is sacred.

Quarterly payments (US)

Self-employed people owing $1,000+ in federal tax must make quarterly estimated payments (Apr 15, Jun 15, Sep 15, Jan 15). Your tax account funds these payments. State estimated payments may also apply. Missing quarterly payments triggers underpayment penalties.

Quarterly installments (Canada)

Self-employed Canadians owing over $3,000 in combined federal+provincial tax must make quarterly installments (Mar 15, Jun 15, Sep 15, Dec 15). CRA bills these automatically based on prior year; your tax account pays them.

Handling Irregular Expenses

Irregular income means you cannot cover annual expenses from that month's paycheck. Use sinking funds — small monthly transfers that accumulate for annual costs.

Example sinking funds

-

Car insurance renewal ($1,800/year): $150/month

-

Holiday gifts ($1,200 total): $100/month

-

Vacation ($3,000/year): $250/month

-

Computer replacement ($2,000 every 3 years): $55/month

-

Professional development ($1,200/year): $100/month

Fund sinking funds from your personal salary, the same way a salaried employee would. The business account does not pay them directly.

When Cash is Tight

Even with a buffer, some months are going to be tight. The decision tree:

-

Has the buffer lasted 2+ months of below-average income? Yes → review whether your salary is set too high

-

Is this a normal slow season? Yes → trust the buffer, do nothing

-

Is this a permanent income decline? Yes → cut the salary by 10-20% and rebuild the buffer

-

Is this a short-term shock (lost a big client, medical issue)? Yes → reduce personal discretionary spending temporarily, protect the buffer

The biggest mistake in a tight stretch is giving up on the system and reverting to 'whatever lands this month, I spend this month.' Stay with the system. The whole point of the buffer is that you are insulated from the bad month.

Getting Paid Late

The irregular-income problem is not just variable revenue — it is often variable timing. You invoice $5,000 in March, and it might arrive in April, June, or never.

The buffer fixes timing problems, but only if you avoid these two traps:

-

Do not count invoiced work as income until the money arrives. An $8,000 invoice is worth zero dollars of spendable cash until the client pays.

-

Do not stretch the tax reserve to cover late payments. If a client pays late and leaves you with $5,000 short this quarter, pull from the buffer — not the tax account.

Upgrading the System Over Time

Once the basic four-account system is humming, typical upgrades as income and consistency grow:

-

Year 1: 2-month buffer, simple percentages, quarterly tax payments

-

Year 2-3: 3-month buffer, annual salary increases based on documented growth, real accounting software (Xero, QuickBooks Self-Employed)

-

Year 4+: Incorporation in many cases, formal payroll, separate accounts for business taxes vs personal taxes, working with a bookkeeper and accountant

The Real Benefit

The tangible benefit of this system is that you know what you can spend every month. But the deeper benefit is psychological. Freelancers who live month-to-month on whatever lands that month are stressed even when revenue is high — there is always the next lean month coming. Freelancers with a buffer and a stable salary stop panicking about every slow invoice and start making better business decisions, because the day-to-day cashflow noise is no longer an emergency.

Start with one month of buffer if that is all you can manage. Get to two. Get to three. Somewhere in there, you will notice you stopped checking your bank balance three times a day — that is the real goal.

Use the free Cashflow Planner on spnd.io to map out your variable income and set your salary amount with confidence. Works for any pay frequency, any income range, any currency.