Most budgeting advice defaults to monthly — you plan a month in advance, check a month later, and adjust. Monthly has been the default for decades because bills come monthly. But monthly cadence does not match how most people actually experience money — most people feel flush on Friday and broke on Wednesday.

This guide compares the two cadences, identifies who each works for, and explains how to pick — or combine — them in a way that actually survives past the first payroll.

Why Monthly Became The Default

Monthly budgeting matches the calendar of bills. Rent, mortgage, utilities, subscriptions, insurance — nearly every recurring expense arrives on a monthly cycle. A month is also long enough to average out the randomness of day-to-day spending, so the picture is cleaner. And in a pre-digital era, bank statements came monthly — you literally could not see your spending more often than that.

None of that is wrong. But the world has changed, and the cadence that matches reality now is not necessarily monthly.

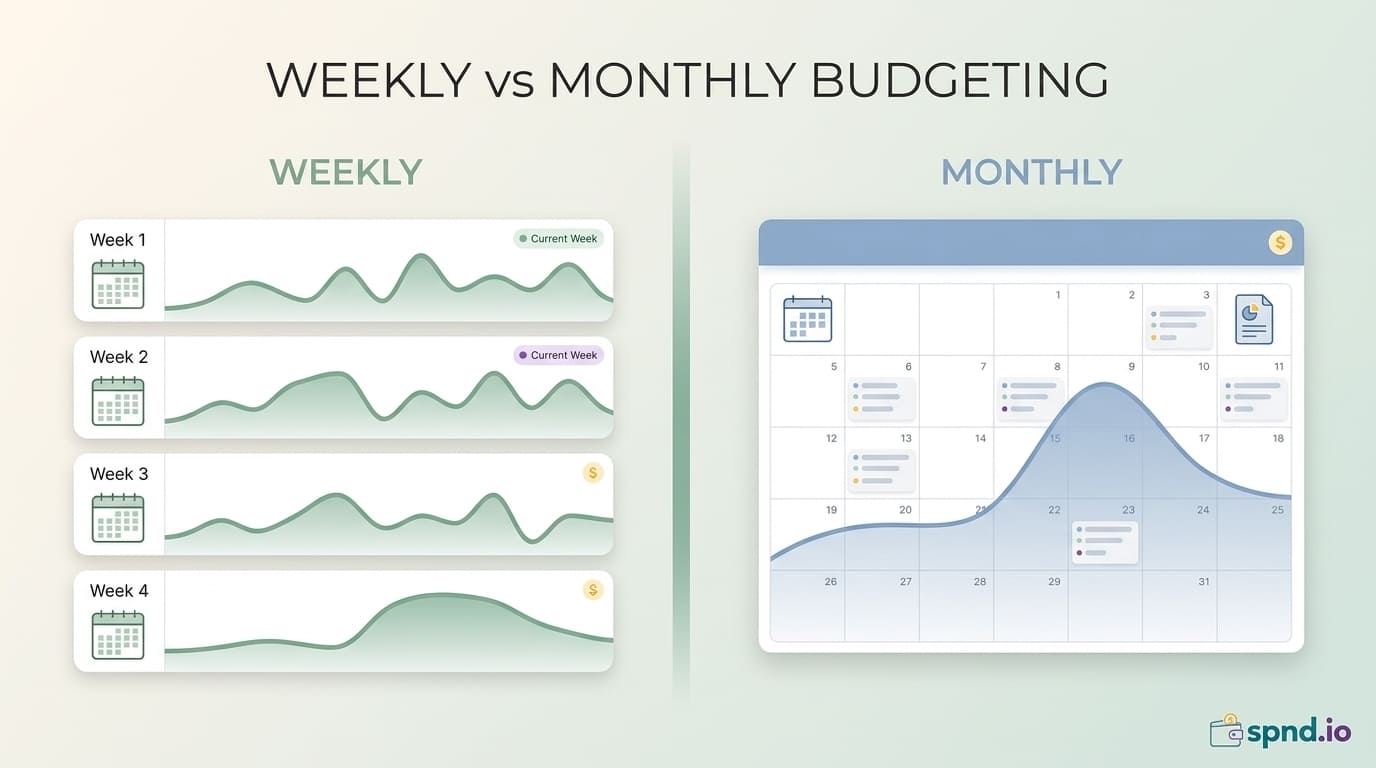

Weekly Cashflow Planning: How It Works

Instead of planning a full month at a time, you plan one week at a time. On Sunday night (or whenever your week resets), you look at:

-

Cash on hand today

-

Income arriving this week

-

Bills and expenses due this week

-

Planned discretionary spending this week

-

Savings/debt transfer for this week

You end with a clear weekly spending allowance for groceries, fun money, and gas. That allowance refreshes every week.

Who Should Plan Weekly

You get paid weekly or bi-weekly

If paychecks hit every week or two, a monthly plan creates mental arithmetic you do not need. Your money lives in weekly chunks — plan it that way.

Your income is variable

Freelancers, gig workers, commission-based salespeople, servers working tips, anyone whose paycheck varies week to week. Monthly budgets assume stability you do not have. Weekly planning lets you absorb each paycheck's reality as it arrives.

You run out of money before the end of the month

The most common budgeting failure: overspending in weeks 1 and 2 because the paycheck feels like a lot, then scraping in weeks 3 and 4. Weekly planning makes the end-of-month crunch impossible because you cannot overspend the week's allowance without feeling it immediately.

You're paying down debt aggressively

Weekly check-ins keep you accountable and let you adjust quickly if a week goes sideways. Monthly budgeting means you realize 3 weeks too late that you overspent.

Who Should Plan Monthly

You're salaried with one monthly paycheck

Twice-a-month or monthly salary, predictable bills, stable life. A monthly cadence matches the rhythm of your actual finances — no benefit to chopping it finer.

Your expenses are all fixed and automated

Rent auto-pays, utilities auto-pay, subscriptions auto-pay, transfers to savings auto-pay. Almost all your money moves without you doing anything. You do not need weekly check-ins for a system that does not require weekly decisions.

You find weekly planning exhausting

If you tried weekly and burned out within a month, monthly is better for you. A monthly plan you do consistently beats a weekly plan you abandon.

Head-to-Head Pros and Cons

Weekly — strengths

-

Much faster feedback loop on overspending

-

Matches paycheck rhythm for hourly/bi-weekly earners

-

Makes 'coasting to payday' psychologically impossible

-

Easier to adjust when life changes suddenly

-

More realistic for variable incomes

Weekly — weaknesses

-

More time commitment — 15-30 minutes each week

-

Hard to see monthly patterns (some expenses only happen once a month)

-

Annual and seasonal expenses are harder to plan for

-

Can feel like you are constantly thinking about money

Monthly — strengths

-

Matches how bills actually arrive

-

Less time spent — 30-60 minutes once a month

-

Easier to see patterns and averages

-

Natural fit for salaried earners with stable income

Monthly — weaknesses

-

Slow feedback — overspending in week 1 not caught until week 4

-

Relies on self-discipline to pace spending across 4 weeks

-

Breaks down for variable or weekly incomes

-

Can create false confidence because the 'big' number looks healthy until late in the month

The Hybrid: Monthly Strategy, Weekly Execution

For most people, the best answer is not 'one or the other' — it is both, at different levels.

Monthly level

Set your targets: how much for rent, utilities, groceries, dining out, gas, savings, debt, etc. Decide once a month what the numbers should be. Automate the fixed expenses. Set the savings/debt transfers on payday. This work takes 30-45 minutes once a month.

Weekly level

Execute on the discretionary categories weekly. Grocery budget for the month? Divide by 4, see how you are doing each week. Fun money? Divide it weekly so you do not blow through it in week 1. Each Sunday, 10 minutes: check where you are, adjust for the week ahead.

This structure gives you the stability of monthly planning and the discipline of weekly tracking. It is what most successful budgeters actually do once they have been at it for a year or two, even if they do not call it by this name.

A Quick Tool: The Weekly Number

If weekly planning sounds overwhelming, there is a lightweight version that most people can sustain.

Take your monthly discretionary spending target (groceries + dining + fun money + gas, anything that varies). Divide by 4.33 (number of weeks in a month). That is your 'weekly number.'

Every Sunday, open your banking app, look at how much you spent in those categories in the past 7 days. Compare it to your weekly number. If you are under, great. If you are over, the next week's budget is tighter. That is the whole system.

No spreadsheets. No detailed categorization. Just one number per week. This beats the full monthly approach for most people who have tried monthly and failed.

Common Mistakes Regardless of Cadence

-

Not writing anything down — both cadences require a system, not just a thought

-

Not accounting for irregular expenses (annual insurance, holiday gifts, car registration) — use sinking funds regardless of weekly/monthly

-

Rebuilding the whole plan every period — set your percentages once, tweak rarely

-

Reviewing only when things feel good — consistency matters more than motivation

How to Decide For Yourself

Three questions to settle it:

-

How often do you get paid? Weekly/bi-weekly → weekly planning. Monthly/semi-monthly → monthly planning.

-

Is your income stable or variable? Stable → monthly. Variable → weekly.

-

Do you tend to overspend before the end of the pay period? Yes → weekly. No → monthly.

Majority of answers points to your cadence. For anyone split down the middle: start with the hybrid approach. It meets you where you are without forcing one extreme.

The Honest Bottom Line

Cadence is a tool for consistency. The best cadence is the one you will actually maintain, not the one that sounds most rigorous. A monthly plan you check every week is fine. A weekly plan you do for three weeks and abandon is worse than no plan.

Start with what fits your paycheck rhythm, use the weekly-number shortcut if you are new to it, and graduate to the hybrid once it feels natural. Every system you stick with for a year beats every perfect system you quit in a month.

Ready to try either cadence? The free Cashflow Planner on spnd.io works equally well for weekly or monthly planning — plug in your income and expenses once, then review at whatever cadence suits you best.