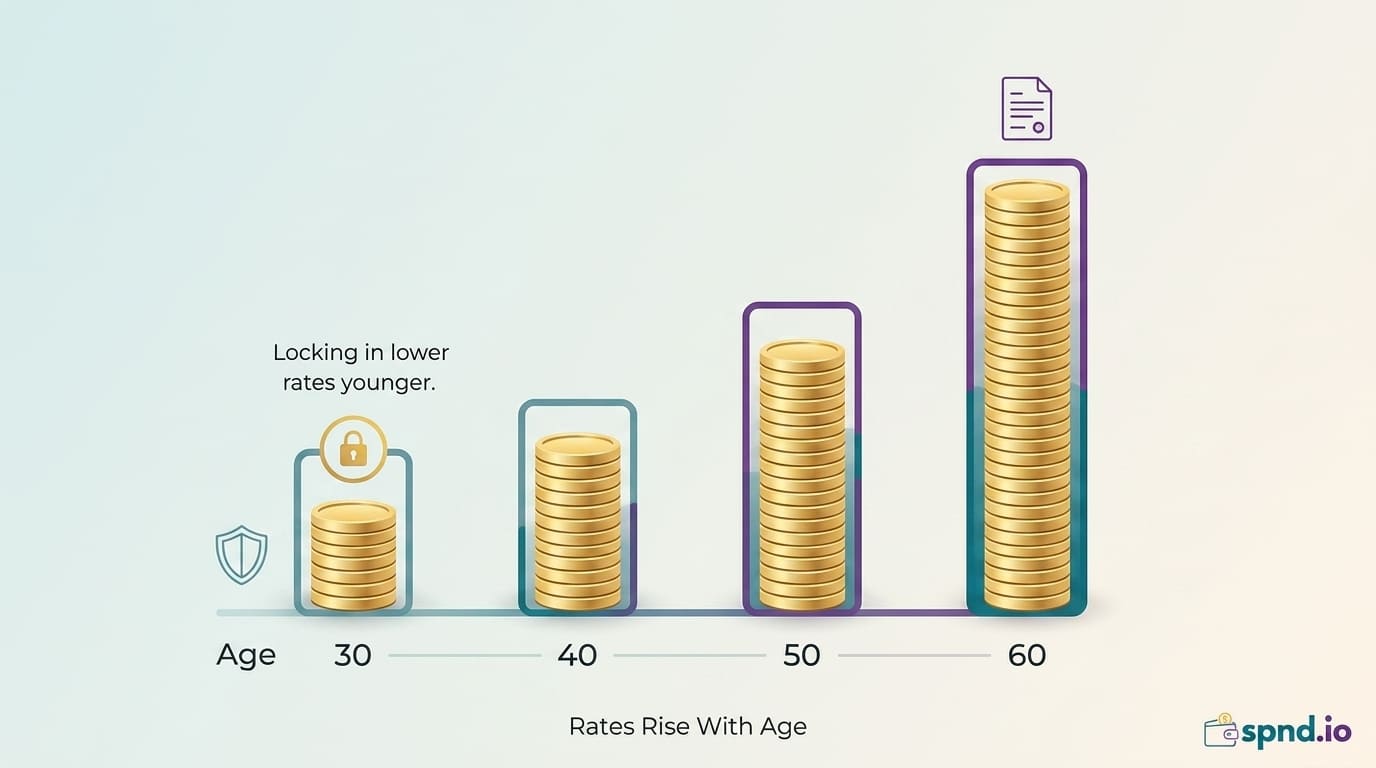

Life insurance gets meaningfully more expensive every year you wait. Not linearly — exponentially. The premium you lock in at 32 is dramatically cheaper than what you'd pay at 42 for the exact same coverage, and the same policy at 52 costs four times as much.

This post shows real 2026 term life insurance rates by age, gender, and coverage amount, explains the factors that move your price up or down, and helps you figure out what 'good rates for my age' actually look like. All numbers are for healthy non-smokers in the US, with notes on Canadian rate differences.

Why Age Dominates the Price

Life insurance is priced entirely off the probability that you die during the policy term. As you age, that probability rises — slowly at first, then more steeply. An insurer pricing a 20-year term for a 35-year-old needs to cover the possibility of death between ages 35 and 55, which is low. The same 20-year term at age 55 covers ages 55-75, where the probability of death is several times higher.

That is why the price curve is not flat. Every year of waiting compounds on previous years' increases.

Real 2026 Term Rates: $500,000 Coverage

20-year term, healthy non-smoker, US

Age 25

-

Male: $18-22/month

-

Female: $14-18/month

Age 30

-

Male: $20-28/month

-

Female: $16-22/month

Age 35

-

Male: $25-35/month

-

Female: $20-28/month

Age 40

-

Male: $40-55/month

-

Female: $30-42/month

Age 45

-

Male: $60-85/month

-

Female: $45-65/month

Age 50

-

Male: $95-130/month

-

Female: $70-100/month

Age 55

-

Male: $160-230/month

-

Female: $115-170/month

Age 60

-

Male: $260-380/month

-

Female: $185-275/month

Real 2026 Term Rates: $1,000,000 Coverage

20-year term, healthy non-smoker, US

Age 30

-

Male: $35-50/month

-

Female: $28-40/month

Age 35

-

Male: $45-65/month

-

Female: $35-50/month

Age 40

-

Male: $70-100/month

-

Female: $55-78/month

Age 45

-

Male: $115-160/month

-

Female: $85-120/month

Age 50

-

Male: $180-255/month

-

Female: $130-190/month

Age 55

-

Male: $310-440/month

-

Female: $220-325/month

The 10-Year Price Increase in Plain Dollars

The same $500,000 20-year term policy for a healthy male non-smoker:

-

Buy at 30 vs buy at 40: roughly double the monthly premium

-

Buy at 30 vs buy at 50: roughly 5x the monthly premium

-

Buy at 30 vs buy at 60: roughly 13-14x the monthly premium

Lock in the rate young and you are paying the age-30 premium until the policy expires 20 or 30 years later. Wait until 45 and you are paying the age-45 premium for the rest of that policy period.

Canadian Rates: Expect 10-20% Higher

Canadian term life insurance is typically 10-20% more expensive than comparable US policies, due to a smaller market with fewer competitors. Otherwise, the age curve behaves identically.

-

Age 35, $500K 20-year term, healthy male non-smoker (Canada): $30-42 CAD/month

-

Age 45, same: $70-100 CAD/month

-

Age 55, same: $180-270 CAD/month

What Pushes Your Rate Up

Smoking (the single biggest factor after age)

Smokers pay 2-3x the rates of non-smokers at every age. A 35-year-old male non-smoker at $30/month could be paying $90+/month for the identical policy as a smoker.

-

'Smoker' usually means any nicotine use in the last 12 months — cigarettes, cigars, vape, chew, nicotine gum, patches

-

Quitting and staying nicotine-free for 12 months usually qualifies you for non-smoker rates on a new application

-

Worth applying for a new policy after hitting the 12-month milestone even if your existing smoker-rate policy is in force

Health conditions

-

High blood pressure (controlled): +15-30%

-

High cholesterol (controlled): +10-20%

-

Type 2 diabetes (well-controlled): +30-70%

-

Obesity (BMI above 35): +25-60%

-

History of cancer (depends on type, staging, years since treatment): varies widely from +0% to uninsurable

-

Mental health conditions well-managed: minimal or no impact

Family history

Parents or siblings diagnosed with heart disease, cancer, diabetes, or stroke before age 60 can raise premiums 10-25% depending on the specifics and your own health.

Occupation and hobbies

Most desk-based careers are rated standard. Higher-risk occupations (commercial fishing, logging, roofing, certain military roles) and hobbies (scuba diving, private aviation, rock climbing, racing) can increase premiums or require riders.

The 'Rate Class' System

Insurers sort applicants into rate classes. A quote you see online is usually the best rate class — but you may not qualify for it. Typical classes from best to worst:

-

Preferred Plus / Super Preferred: Best rates, ~20% of applicants. Perfect health, ideal weight, no family history.

-

Preferred: Excellent rates, ~25% of applicants. Minor issues like slightly elevated cholesterol or family history.

-

Standard Plus: Good rates, ~20% of applicants. Some health factors present.

-

Standard: Average rates, ~25% of applicants. Common health conditions present and controlled.

-

Substandard / Table ratings: Higher rates, ~10% of applicants. Significant health conditions.

Moving from Preferred Plus to Standard can double your premium. This is why real quotes require a health exam and underwriting — online estimates show you the best-case rate, not your actual rate.

The 'Lock It In Now' Decision

The cost of waiting to buy life insurance is almost always higher than the cost of buying it now, for three reasons:

-

Every year you age, the rate goes up — and the increase gets steeper each year

-

Every year that passes increases the chance you develop a health condition that permanently raises your rates or makes you uninsurable

-

A 30-year term bought at 35 covers you to age 65 — right through the peak need years. The same 30-year term bought at 45 only covers to 75, meaning you might outlive your coverage with dependents still needing support

For the vast majority of people with dependents, the right move is: apply now, lock in the current age's rate, and hold the policy as long as you need coverage. You can always drop a term policy if your situation changes. You cannot retroactively buy it at your younger age after you develop a condition.

Getting Your Actual Rate

The tables above are market averages. Your specific rate depends on your specific health, family history, lifestyle, and the specific carrier you apply with — same applicant can get wildly different quotes from different insurers because each has its own underwriting preferences.

The most cost-effective way to get real rates is to work with an independent broker or platform that compares multiple carriers simultaneously. Applying with one carrier and getting a bad rate is not a market rate — it is that carrier's rate.

Want to see your real rate based on your actual age, coverage needs, and situation? Start with the free Life Insurance Calculator on spnd.io — then, if it makes sense, connect with a licensed broker to get multiple quotes in a single conversation.