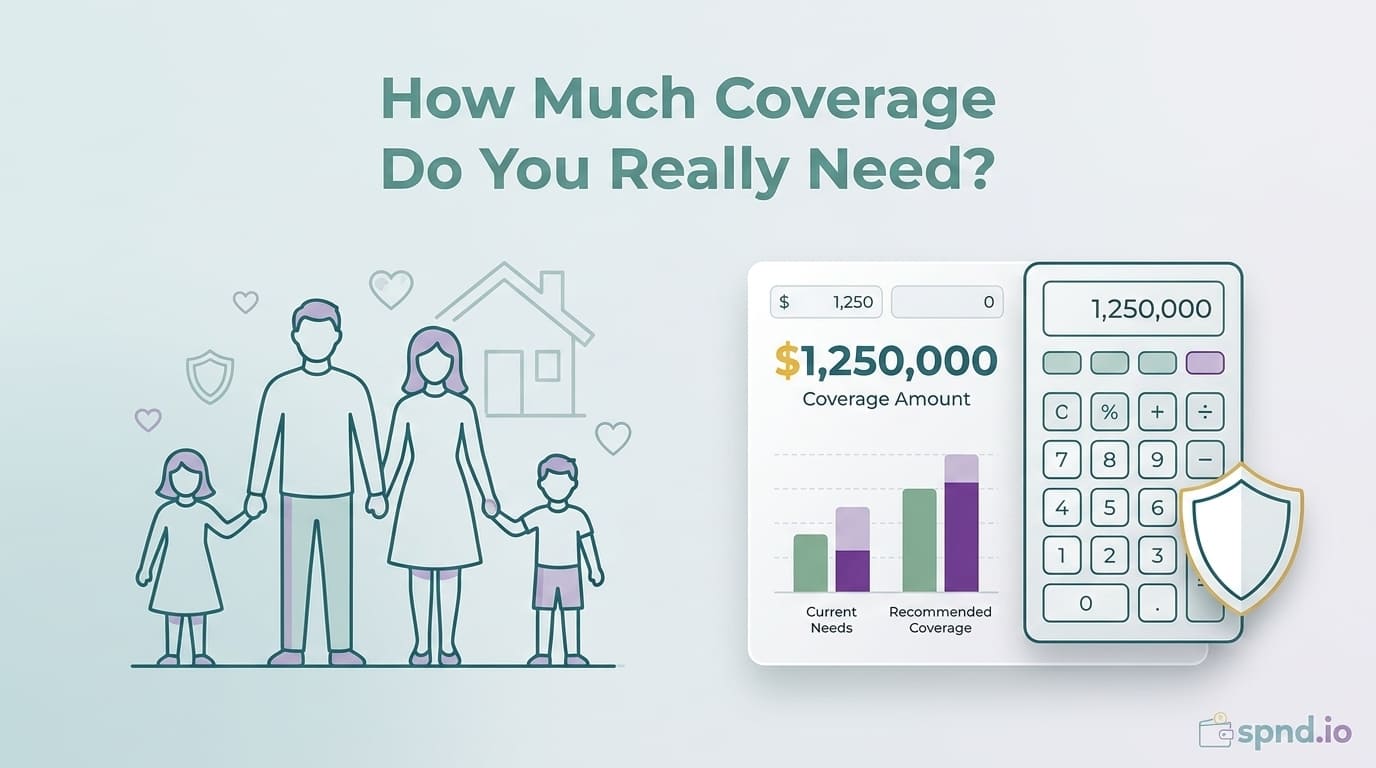

Life insurance is one of those products where the right amount of coverage matters far more than the brand of the policy. Buy too little and your family has to rebuild from a weakened starting point. Buy too much and you are paying premiums for a bigger policy than anyone will actually need.

There are three methods financial planners use to calculate the right coverage amount. This post walks you through all three, tells you which one to use for your situation, and helps you arrive at a real number in under ten minutes.

Who Actually Needs Life Insurance

Before calculating how much, confirm you need it at all. Life insurance exists to replace the financial contribution you make to people who depend on you. If no one relies on your income or unpaid labor, you probably do not need coverage.

You likely need life insurance if

-

You have a spouse or partner who depends on your income

-

You have children — biological, adopted, step, or other dependents

-

You have a mortgage or significant debt co-signed by a partner

-

You are a stay-at-home parent providing childcare and household labor

-

You own a business with partners or employees who depend on you

-

You support aging parents or adult family members financially

You probably do not need life insurance if

-

You are single with no dependents

-

You have no significant debts co-signed with anyone

-

Your assets are already large enough to cover your final expenses and any dependents' future needs

Exception: Young healthy people with no dependents sometimes buy small term policies at young ages purely to lock in insurability — meaning if they develop a health condition later, they can still convert or expand coverage. This is optional and not a necessity.

Method 1: Income Replacement (The 10x Rule)

The simplest method, and the one most often cited. Multiply your annual gross income by 10-12. That is your starting coverage number.

When to use it

-

You are employed with a steady income

-

You want a quick estimate without a lot of inputs

-

Your situation is relatively straightforward (no business ownership, no unusual debts)

How it works

-

$50,000 income → $500,000-$600,000 coverage

-

$100,000 income → $1 million-$1.2 million coverage

-

$150,000 income → $1.5 million-$1.8 million coverage

The logic: if the survivor invests the lump sum at a conservative 4% annual return, it generates roughly the deceased person's income indefinitely without touching the principal. A 10x multiplier gives about 20 years of income replacement with some erosion; 12x gives closer to 25 years.

Limitations

The 10x rule does not account for specific debts, specific education goals, or existing assets. Two people with the same income often need wildly different coverage. Use this as a starting point and refine with one of the other methods.

Method 2: DIME (Debt, Income, Mortgage, Education)

A more tailored approach. Add up the four categories and that is your coverage need.

D — Debt

All outstanding debts your family would inherit or become responsible for: credit cards, student loans (depends on type and country), car loans, personal loans, and any co-signed debt. Exclude the mortgage — that is counted separately.

I — Income

Annual gross income multiplied by the number of years the family needs replacement. Common assumption: cover until the youngest child turns 22, or 15-20 years, whichever is longer. A 35-year-old with a 3-year-old might target 19 years of income replacement. At $80,000/year income, that is $1.52 million.

M — Mortgage

Current outstanding mortgage balance. The logic is that the surviving partner can use the death benefit to pay off the house entirely, removing the single largest fixed expense. Not everyone agrees with this — some prefer to keep the mortgage and invest the difference — but it is the traditional DIME approach.

E — Education

Estimated future education costs for all children. Rough 2026 numbers:

-

US in-state public university (4 years): $100,000-$130,000

-

US private university (4 years): $250,000-$350,000

-

Canadian undergraduate (4 years): $60,000-$100,000 CAD

Multiply by the number of children and subtract any existing 529 or RESP balances.

DIME example

A 35-year-old with $80,000 income, spouse, two kids (ages 3 and 6), $250,000 remaining mortgage, $20,000 in student loans, $15,000 in car loans:

-

Debt: $35,000

-

Income: $80,000 × 19 years = $1,520,000

-

Mortgage: $250,000

-

Education: 2 kids × $115,000 = $230,000

-

DIME total: $2,035,000

Round to $2 million coverage. That is significantly higher than the 10x rule would suggest ($800,000-$960,000). This is typical — the DIME method usually produces larger numbers than income replacement because it accounts for specific life costs.

Method 3: Needs-Based Calculation

The most accurate and most time-intensive. Build up from actual annual household needs and subtract existing resources.

Step 1: Calculate ongoing annual needs

What would the surviving household actually spend per year? Start with current household expenses, then remove the deceased's personal costs (food, clothing, transportation, hobbies). A good estimate is 70-80% of current spending.

Step 2: Calculate one-time needs

Funeral costs ($7,000-$15,000), final medical expenses, mortgage payoff (optional), debt payoff, and education fund.

Step 3: Subtract existing resources

-

Existing savings and investments

-

Retirement account balances

-

Social Security survivor benefits (US) / CPP survivor benefit (Canada) — rough estimate of annual amount × years

-

Existing life insurance through employer

-

Surviving partner's expected income

Step 4: Calculate the gap

The total needs minus the existing resources is your coverage gap. Target coverage should equal the gap, plus a 10-15% cushion for inflation, investment underperformance, or unexpected costs.

This method usually produces a number between the 10x rule and DIME — sometimes lower, sometimes higher — but it is specific to your actual situation. Recommended for anyone with complex finances or substantial existing assets.

Which Method Should You Use?

-

10x rule: If you want a fast starting estimate and have a simple financial situation

-

DIME: If you have a mortgage and children — this is the best middle-ground approach for most families

-

Needs-based: If you have significant assets, are self-employed, have a complex family structure, or want the most accurate number

The most practical approach: calculate using all three. If they agree within 20%, pick the DIME number and move on. If they disagree significantly, use the needs-based method or talk to an insurance professional to understand the gap.

Don't Forget: Stay-at-Home Parents Need Coverage Too

One of the biggest mistakes in life insurance planning. A stay-at-home parent's unpaid labor is economically enormous — childcare, cooking, cleaning, scheduling, transportation, household management. Replacing those services professionally costs $45,000-$75,000 per year depending on the region.

A stay-at-home parent should typically have $500,000-$750,000 of term coverage, regardless of zero reported income. This protects the working partner from the career-altering costs of handling everything alone.

Term vs Permanent: Quick Note

For 90% of people, term life insurance is the right answer. It covers you for a fixed period (10, 15, 20, 25, or 30 years), is 5-15x cheaper than permanent insurance for the same coverage, and matches the time window when your family actually needs protection (while kids are growing up and the mortgage is outstanding).

Permanent life insurance (whole life, universal life) has specific use cases — estate planning for high-net-worth individuals, guaranteed insurability concerns, or specific tax strategies — but is rarely the right tool for basic family protection. Buy term, invest the difference, and by the time the term ends you should have enough assets that you are self-insured.

Getting Your Real Number

The coverage amount matters more than any other decision about life insurance — more than the carrier, the policy type, or the riders. Run your numbers through at least one of the three methods above, then run them again in 2-3 years as your family grows and your finances change.

The cheapest way to be badly protected is to have a policy. The only way to be well protected is to have the right policy. Do the calculation once, seriously, and then go get quotes.

Get your real coverage number in 2 minutes. The free Life Insurance Calculator on spnd.io runs the DIME method with your actual numbers — and if you want to connect with a pre-screened insurance professional for quotes, that is one click away.