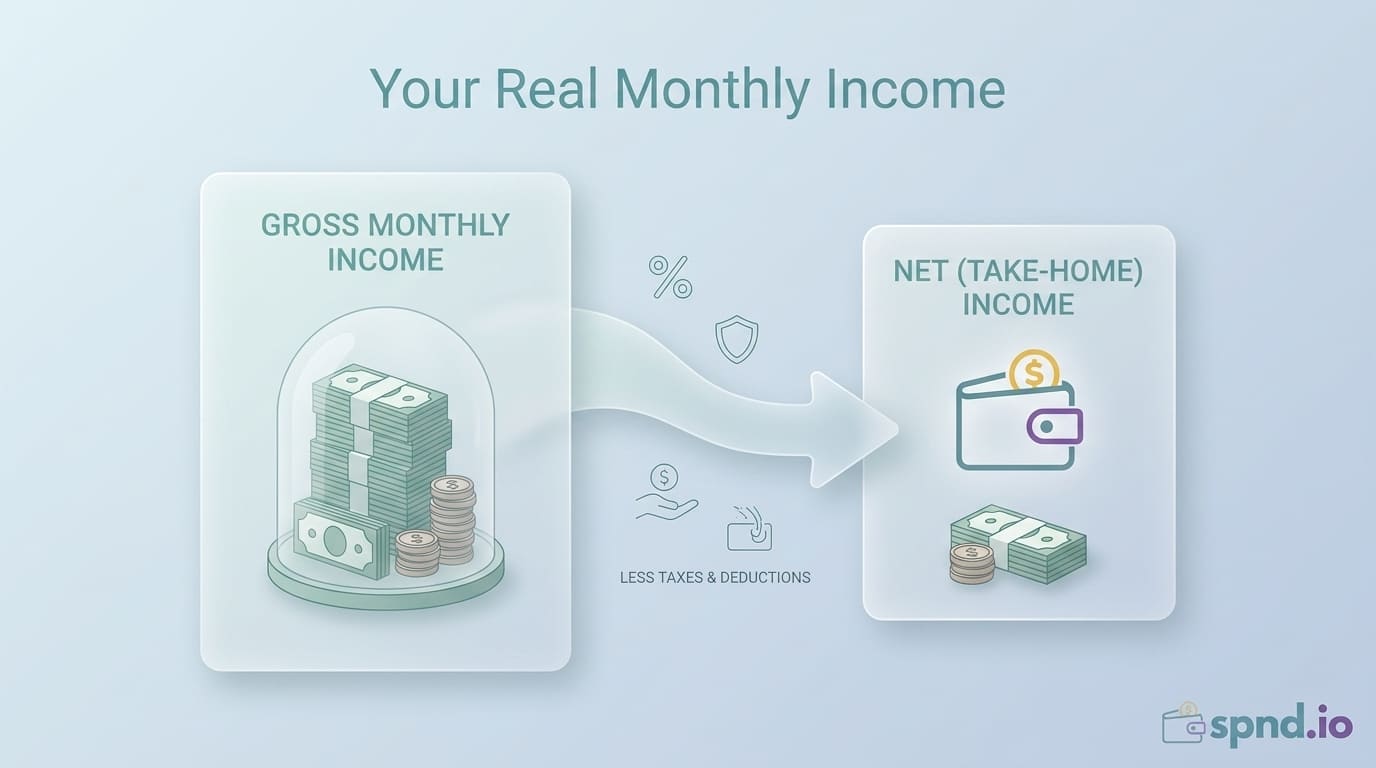

How to Calculate Your Net Monthly Income (USA & Canada)

Your net monthly income — what actually lands in your bank account — is the foundation number for every financial decision you make. Budget percentages run off it. Loan qualification runs off it. Rental applications ask for it. Every financial calculator assumes you know it.

And most people estimate it wrong. This guide walks through exact calculations for the four common situations: salaried, hourly, self-employed, and multiple-income, with the math that applies in both the US and Canada.

Gross vs Net vs Take-Home: The Distinctions

-

Gross income: Before any deductions. The number on your offer letter. Almost never useful for personal budgeting.

-

Net income (tax purposes): Gross minus tax deductions and credits. A calculation the government cares about.

-

Take-home pay (what this article means by net): Your gross minus all mandatory deductions — taxes, Social Security/CPP, Medicare/EI, mandatory insurance. The actual money that hits your bank.

In casual use, 'net income' usually means take-home. That is how we use it here.

Method 1: Salaried Employees (Easiest)

If you have a recent pay stub

-

Find the 'Net pay' or 'Take-home' line on your most recent pay stub.

-

Multiply by your pay frequency: 26 for bi-weekly, 24 for semi-monthly, 12 for monthly, 52 for weekly.

-

Divide by 12. That is your monthly net income.

Example

-

Bi-weekly net pay: $2,100

-

Annual net: $2,100 × 26 = $54,600

-

Monthly net: $54,600 ÷ 12 = $4,550

Important: Bi-weekly pay produces 26 checks per year, not 24. This means 2 months per year have 3 paychecks. Do not use one of those 3-check months as your baseline — it overstates monthly income.

If you don't have a pay stub

Use a net pay calculator. Input gross annual salary, filing status, state/province, and pre-tax deductions (401k, RRSP, health insurance). The calculator outputs estimated annual net — divide by 12 for monthly.

Method 2: Hourly Workers

If hours are consistent week to week:

-

Average hours per week × hourly rate = weekly gross

-

Multiply by 52 for annual gross

-

Subtract estimated taxes using a payroll calculator

-

Divide by 12 for monthly net

If hours vary week to week:

-

Pull the last 3 months of pay stubs

-

Sum the net pay across all stubs

-

Divide by 3 to get monthly average

For budgeting purposes, use the lowest of the three months as your planning number. Treat amounts above that as bonus savings — it removes the panic of a slow month and accelerates savings in good months.

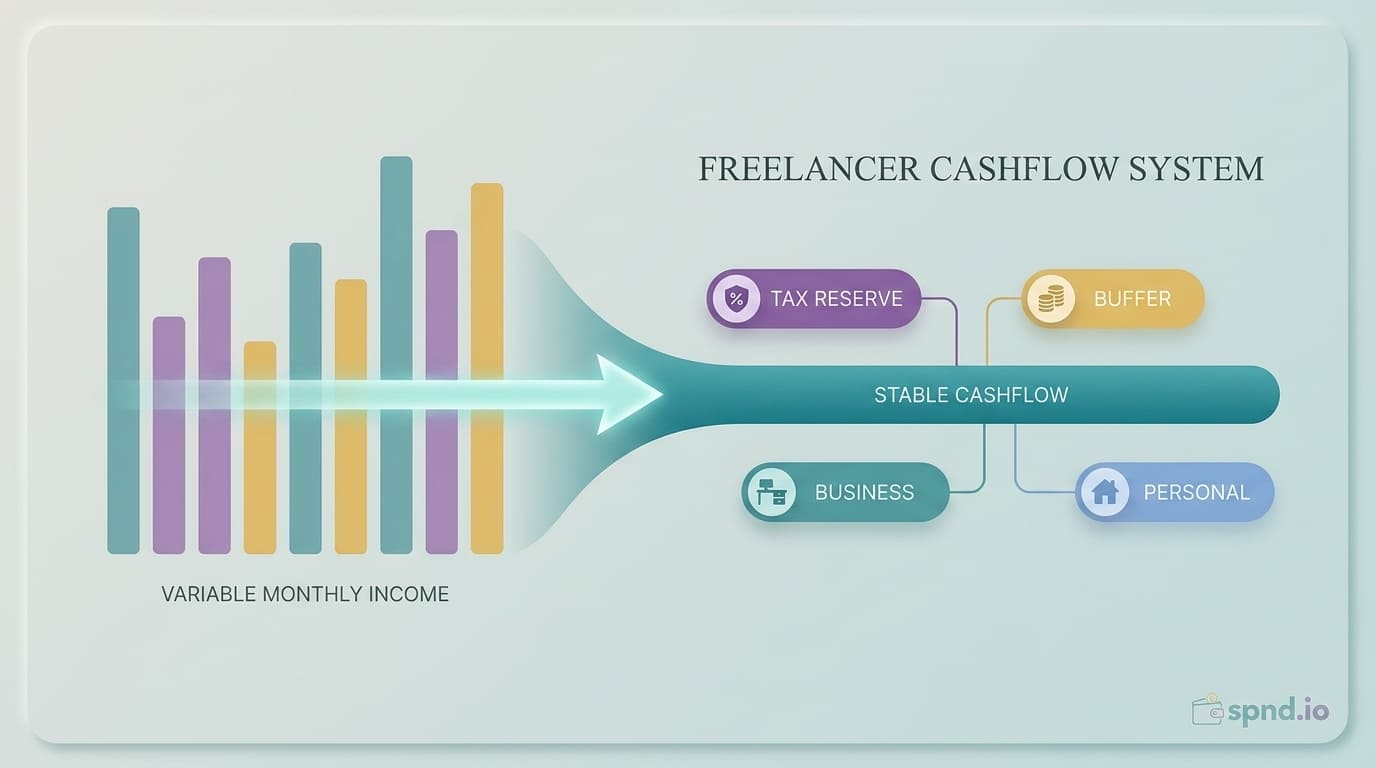

Method 3: Self-Employed / Freelance

This is harder because no employer is withholding taxes. Your gross and net are both responsibilities you manage.

Step 1: Calculate annual business net

Sum all business revenue for the last 12 months. Subtract all business expenses. What remains is your business's net income. This is your personal gross — before personal taxes.

Step 2: Subtract personal tax estimate

Self-employed people pay both income tax and self-employment tax (US) or CPP contributions at the higher rate (Canada). Reasonable estimates:

-

US self-employed at $50K-$100K business net: 25-28% of business net goes to combined taxes

-

US self-employed above $100K: 28-32%

-

Canadian self-employed at $50K-$100K: 25-30% (varies by province)

-

Canadian self-employed above $100K: 30-38%

Step 3: Subtract retirement and health contributions

If you contribute to SEP-IRA, Solo 401(k), or RRSP from business income, and if you pay health insurance premiums from business income, subtract those amounts.

Step 4: Divide by 12

What remains, divided by 12, is your monthly net income. For actual cashflow planning, see our guide on cashflow planning for irregular income.

Example

-

Annual business net: $85,000

-

Tax reserve (27%): $22,950

-

SEP-IRA contribution: $8,500

-

Health insurance paid from business: $6,000

-

Personal net: $47,550

-

Monthly net: $3,960

Method 4: Multiple Income Sources

Common in modern life — W-2 job plus side gig, or two part-time jobs, or one person salaried and a spouse self-employed.

The mistake most people make

Calculating each income source separately and adding them up. The problem: taxes are calculated on combined income, and adding a second income often pushes you into a higher marginal bracket. Your second job's take-home is usually 5-10% lower than you would expect from the first job's tax rate.

The right approach

-

Sum gross income from all sources

-

Use a combined income tax calculator (not separate calculators)

-

Include all pre-tax deductions from all sources

-

Output is combined annual net

-

Divide by 12 for monthly

Household example

-

Partner A salary: $72,000

-

Partner B self-employed net: $38,000

-

Combined gross: $110,000

-

After combined federal + state + FICA for A, self-employment tax for B: ~$78,500

-

Monthly household net: $6,540

Special Considerations

Variable bonuses and commissions

Do not include irregular bonuses in your monthly net income for budgeting purposes. Base your budget on guaranteed income only. Treat bonuses as separate lump sums when they arrive — typically 80-90% to savings or debt payoff, rest to discretionary.

Stock-based compensation

RSUs (restricted stock units) vested during the year count as ordinary income but are often withheld at a flat rate (22% US) that under-withholds for most people. Do not include planned future vests in your monthly net. Calculate net using a tax calculator that accounts for RSU withholding separately.

Pre-tax benefits

If your employer deducts 401(k) contributions, HSA contributions, health insurance premiums, transit benefits, or other pre-tax amounts before you see your net pay, your net is already reduced by those amounts. Do not subtract them again in a budget.

Post-tax deductions

Roth 401(k) contributions, voluntary life insurance premiums, disability insurance, and similar post-tax deductions come out after taxes but before the 'net pay' line on your stub. These are already excluded from your net — again, do not double-subtract.

Why Getting This Right Matters

Every financial calculation flows from monthly net income:

-

The 50/30/20 rule splits your net, not your gross. Using gross overstates every category by 20-30%.

-

Loan affordability (mortgages, auto loans) is based on gross income for qualification but your own life is lived on net.

-

Rental applications typically require income 3x the rent — they mean gross, but your ability to actually afford that rent is based on net.

-

Savings rate percentage is calculated off net income. Saving 20% of gross sounds great but is only 14-16% of what you actually have.

Spending a few minutes getting the number right is probably the highest-leverage financial task of the year. Every other calculation gets either confirmed or corrupted by this one input.

When to Recalculate

-

Every January (new tax year, possible bracket changes)

-

When you get a raise

-

When you change jobs

-

When you change states or provinces

-

After major life events (marriage, divorce, new child, retirement)

-

If benefits change (new health plan, new pre-tax deductions)

Skip the manual math. The free Net Income Calculator on spnd.io handles all four scenarios — salaried, hourly, self-employed, and multi-income — for every US state and Canadian province. Real numbers in under a minute.