There are two main strategies for paying down multiple debts, and the personal finance world has been arguing about them for years. The math people say 'avalanche always wins.' The behavior people say 'snowball always wins.' Both are partially right.

This post breaks down the two methods with real numbers, shows exactly how much each one saves in different scenarios, and tells you which one fits your situation — because for most people, the best method is the one you actually complete, not the one that looks best on a spreadsheet.

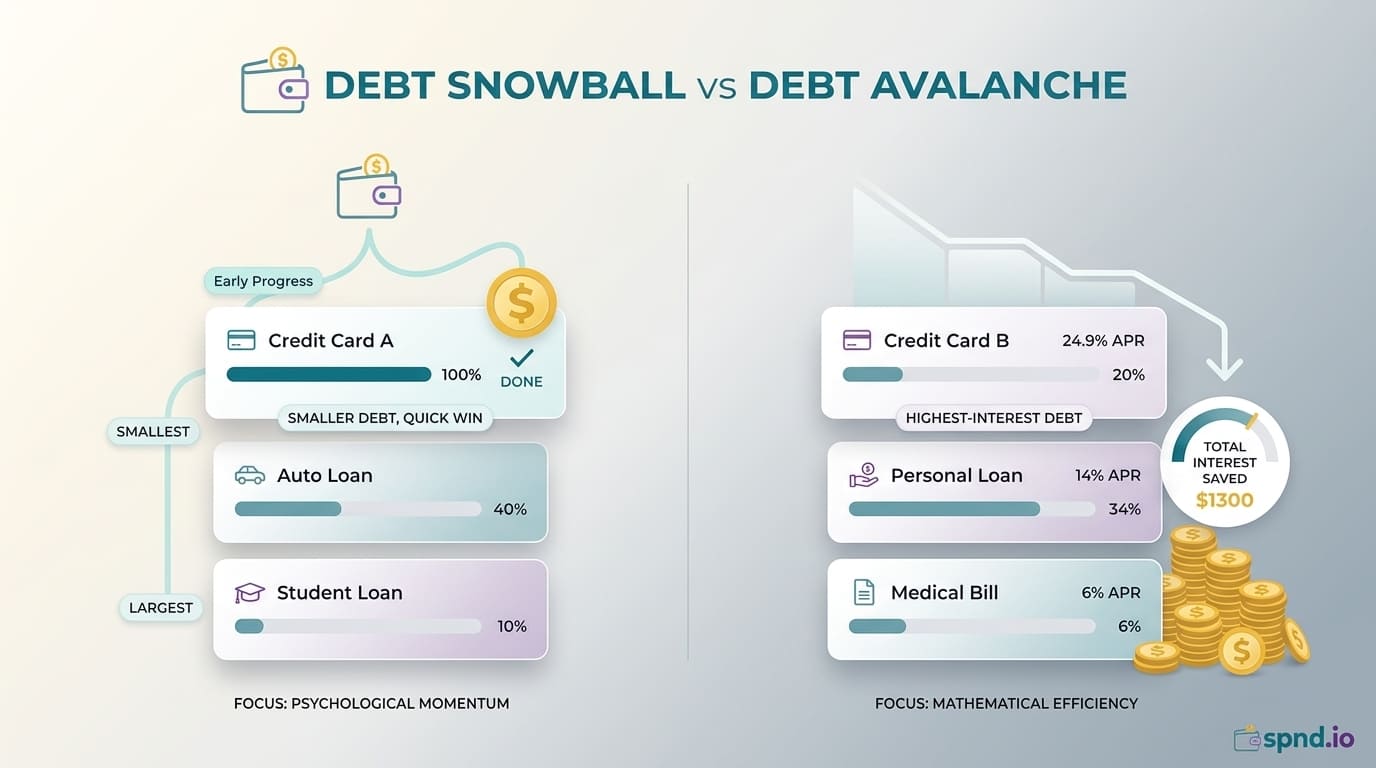

The Debt Snowball Method

Order your debts from smallest balance to largest, regardless of interest rate. Pay the minimum on every debt. Throw every extra dollar at the smallest balance until it is gone. Then roll that payment into the next smallest, and so on.

The logic

Small wins build momentum. Paying off a $600 store card in 2 months feels like a victory, and that victory makes you more likely to stick with the larger debts. Behavioral finance research consistently shows that people who use the snowball method complete their debt payoff at higher rates than people who use the avalanche, even though the avalanche is mathematically faster.

Popularized by

Dave Ramsey's Total Money Makeover. It is the default method in most mainstream personal finance teaching because of its psychological traction.

The Debt Avalanche Method

Order your debts from highest interest rate to lowest, regardless of balance. Pay the minimum on every debt. Throw every extra dollar at the highest-rate debt until it is gone. Then roll that payment into the next highest rate, and so on.

The logic

Interest is what makes debt expensive. Every dollar of extra payment toward a 24% credit card saves more in future interest than the same dollar paid toward a 6% student loan. Mathematically, the avalanche always produces the lowest total interest paid and the fastest total payoff.

Popularized by

Most traditional financial planners and academic personal finance frameworks. Favored by spreadsheet-minded payers who value the math.

Real Example: Same Debts, Both Methods

Imagine someone with:

-

Store credit card: $800 balance, 26% APR, $25 minimum

-

Visa: $4,500 balance, 22% APR, $95 minimum

-

Personal loan: $3,200 balance, 12% APR, $120 minimum

-

Student loan: $12,000 balance, 6% APR, $135 minimum

Total: $20,500 in debt. Total minimum payments: $375/month. They decide to add an extra $400/month, for a total debt payoff budget of $775/month.

Snowball order (smallest balance first)

-

Store card ($800)

-

Personal loan ($3,200)

-

Visa ($4,500)

-

Student loan ($12,000)

Avalanche order (highest rate first)

-

Store card (26% APR)

-

Visa (22% APR)

-

Personal loan (12% APR)

-

Student loan (6% APR)

Results

-

Snowball: paid off in 33 months, total interest paid ~$2,850

-

Avalanche: paid off in 32 months, total interest paid ~$2,510

-

Avalanche saves: 1 month and $340

In this example, the avalanche wins by about $340 total and a single month. That is real money, but it is not nearly the 'avalanche is always much faster' margin some people imagine. The gap depends heavily on how different the interest rates are and how varied the balances are.

When the Gap Is Bigger

The avalanche advantage grows when:

-

You have a wide spread of interest rates (a 4% mortgage and a 29% credit card)

-

The highest-rate debt is also the largest balance

-

The total debt is large ($50,000+)

In extreme cases the avalanche can save thousands over the snowball. In typical consumer debt cases, the difference is a few hundred dollars over 2-3 years.

When the Gap Is Smaller (or Zero)

-

When your debts have similar interest rates

-

When your smallest debt is also your highest rate (both methods converge)

-

When you're paying off quickly and interest compounds less

The Behavioral Research

Academic studies on debt payoff behavior (Gal and McShane's 2012 research at Kellogg is the most cited) consistently find that people who use the snowball method are more likely to complete their debt payoff. The effect size is large — snowball users in these studies completed roughly 15-35% more frequently than avalanche users in comparable situations.

The mechanism is psychological. Closing out a debt entirely — taking the account from 'balance' to 'zero' — produces a measurable motivational boost. That boost leads people to stick with the plan and find additional dollars to throw at the next balance. Avalanche users, whose first debt often takes longer to pay off (because the highest-rate debt might also be larger), are more likely to lose momentum and quit.

Which One Should You Pick?

Pick the snowball if

-

You have multiple debts and need to see progress to stay motivated

-

Previous debt payoff attempts have failed because you lost steam

-

Your smallest debt is small enough to pay off within 2-3 months

-

You respond emotionally to 'closed accounts' — seeing one go to zero will power you through

Pick the avalanche if

-

You are mathematically motivated and can stick with a plan that takes longer to show its first 'win'

-

Your highest-rate debt is significantly above your other debts (25%+ credit card vs 4% mortgage)

-

You have a large total debt ($50,000+) where the interest savings are meaningful

-

You have a history of completing long financial projects without external motivation

Hybrid approach

A reasonable middle path: knock out any trivially small balances first (under $1,000 — pay these off in the first 1-2 months regardless of rate), then switch to avalanche for everything remaining. This captures the psychological boost of quick wins and then optimizes the rest for interest savings.

What to Do Before Starting Either Method

-

Stop adding to the debt. Neither method works if you are still using the credit cards. Freeze them, remove them from digital wallets, delete saved payment methods on shopping sites.

-

Build a $1,000 starter emergency fund first. Without one, the first unexpected $500 expense goes back on a credit card and restarts the cycle.

-

List every debt: creditor, balance, minimum payment, interest rate. You cannot attack what you have not inventoried.

-

Calculate your total monthly payoff budget. Minimums + whatever extra you can commit. This is your firepower.

-

Automate the minimums across all debts. Only the 'extra attack dollars' need to be managed manually.

Acceleration Tactics That Work With Either Method

Balance transfer cards

Move high-rate balances to a 0% balance transfer card (typically 12-21 months of no interest, with a 3-5% upfront transfer fee). Every dollar you pay during the 0% period goes entirely to principal. On $10,000 of credit card debt at 22%, a balance transfer can save $1,500-$2,500 over a year — far more than most debt-payoff optimization choices.

Only works if you qualify (typically requires good credit, 680+), pay off within the promo period, and do not add new purchases to the transferred card.

Debt consolidation loan

A personal loan (typically 8-14% APR for good credit) used to pay off multiple higher-rate credit cards. Works best when: you qualify for a rate significantly below your credit card rates, and you avoid running the cards back up. Can shift $15,000 of 22% debt to 10% debt, saving thousands in interest over the payoff period.

Negotiated settlements or hardship programs

If you are severely behind (90+ days), credit card companies sometimes accept negotiated settlements at 40-70% of the balance. This damages credit score and creates a tax liability on the forgiven amount, but may be the right move for someone who cannot realistically pay the full amount. Not a first option — a last-resort option.

The Honest Answer

The 'best' method is the one you will actually finish. If you have tried debt payoff before and quit, try the snowball this time — the behavioral research is overwhelming and the math gap is small. If you are naturally a spreadsheet optimizer and have the discipline to stick with a plan without quick feedback, the avalanche is marginally better.

Either way, the most important choice is to start this week with a specific plan, a specific number, and a specific automated first transfer. Debt does not shrink from good intentions. It shrinks from payments.

The free Credit Card Debt Calculator on spnd.io runs both the snowball and avalanche methods for your actual debts. Enter your balances and rates, see exactly how long each method takes, and pick the path you will actually complete.