Saving Tips

Saving Tips

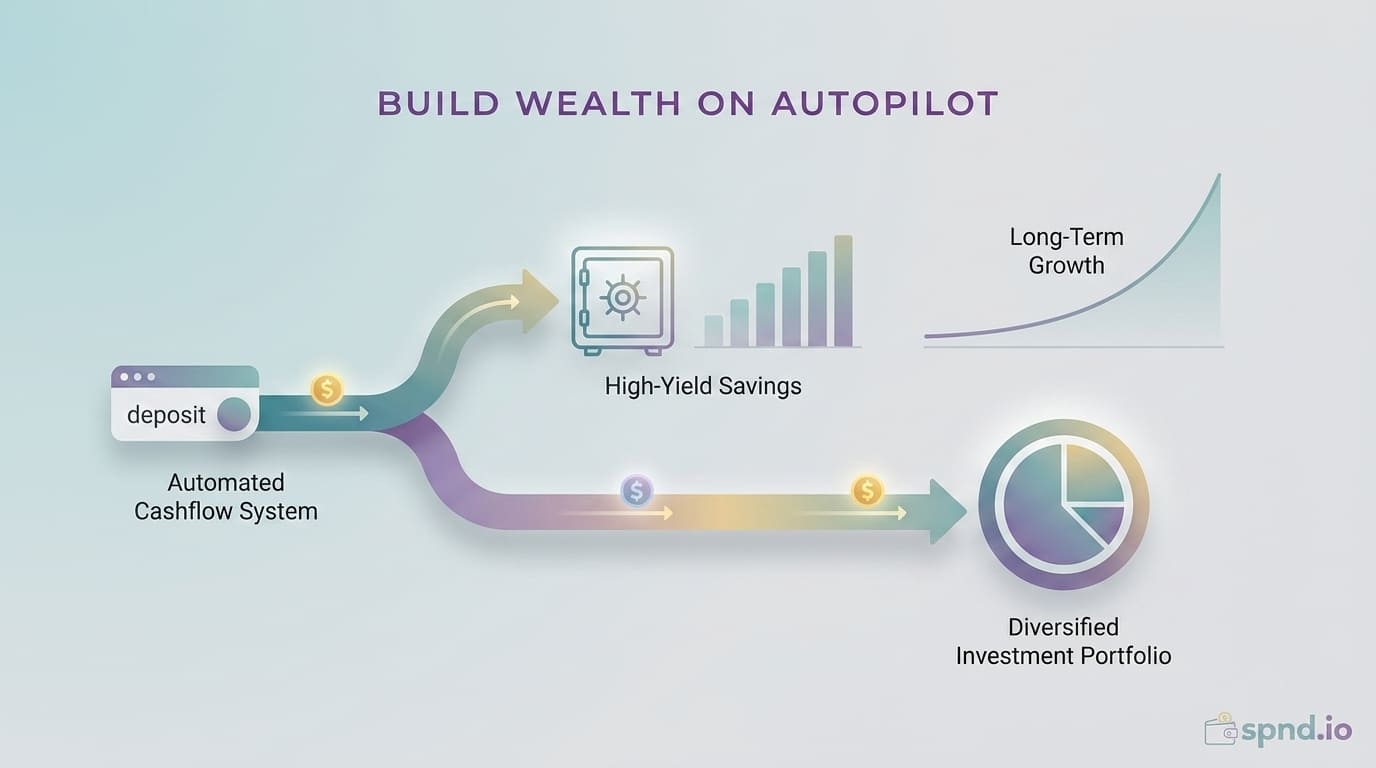

Automation: The Quiet Secret to Building Wealth

Automation is the single biggest predictor of long-term savings success. People who automate transfers to savings and retirement accounts save 2-3x more over a decade than people who rely on manual transfers, because automation removes willpower and decision-making from the equation. Set it up once on payday, and it works for decades.

📅 May 12, 2026

·

🕐 3 min read